Prices at Eight-Month Lows Amid Supply Expansion and Policy Shifts

Executive Summary

Asian fatty alcohol prices have corrected to eight-month lows, down nearly 20 per cent from Q3 2025 peaks, driven by aggressive capacity additions in Indonesia and Malaysia, softer downstream demand, and capped feedstock upside following delays to Indonesia’s B50 biodiesel mandate. While the broader trend remains weak, near-term sentiment has turned firmer on improving demand and renewed export-side uncertainties.

Price Trend Overview (FOB SEA)

- Fatty alcohol C12-C14 prices climbed sharply in Q3 2025, rising from $3,012/MT in August to a peak of $3,170/MT plus in September.

- From October 2025, prices entered a sustained decline, falling to $2,930/MT in October, $2,618/MT in November, and $2,489/MT in December.

- By January 2026, prices stabilised near $2,522/MT, marking a ~20 per cent drop from peak levels and the lowest range seen in eight months.

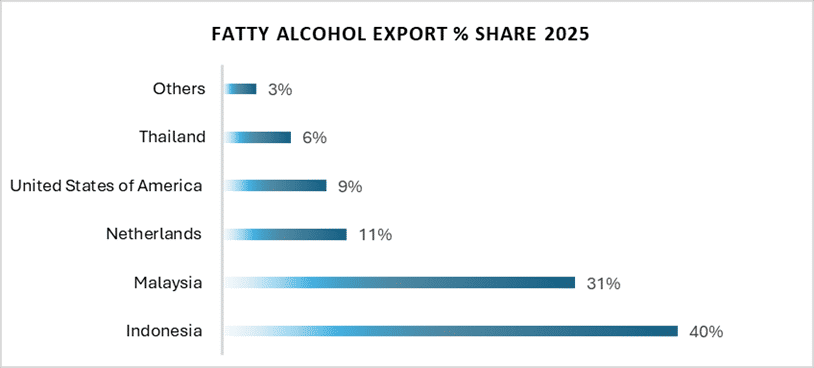

Supply Fundamentals

- New fatty alcohol plants in Indonesia have significantly lifted regional spot availability, particularly for C12–C14 mid-cut grades.

- Higher operating rates and expectations of further capacity additions shifted the market into surplus during Q4 2025.

- Long-chain C16–C18 grades faced additional pressure from competitive offers based on palm stearin feedstock, offsetting cost support from Malaysian Palm Kernel Oil.

Feedstock and Vegetable Oil Dynamics

- Fatty alcohol prices remain linked to movements in Crude Palm Oil (CPO), Palm Kernel Oil (PKO), and palm stearin, though recent pricing has been more supply-driven than cost-driven.

- Palm oil prices typically move in line with other major vegetable oils due to competition within the global edible oils complex.

- PKO and palm stearin pricing is currently shaped more by seasonal output patterns and global vegetable oil balances than biodiesel-related demand.

- Downside risks persist if Indonesian and Malaysian crushing rates remain elevated, increasing exportable feedstock supply.

Indonesia Biodiesel Policy Impact

- Indonesia has postponed the B50 biodiesel rollout to late 2026 or beyond, maintaining the B40 mandate due to technical and funding constraints.

- As a result, incremental CPO demand growth is capped at B40 absorption levels, reducing earlier expectations of tighter feedstock availability.

- The government’s plan to raise palm oil export levies to fund biodiesel subsidies could weaken export competitiveness and introduce volatility into regional trade flows.

Demand Conditions

- Demand from detergent and personal care sectors remains cautious but has shown gradual improvement at lower price levels.

- Buyers continue to follow hand-to-mouth procurement strategies amid macroeconomic uncertainty.

- Oleochemical and industrial consumption remains subdued, limiting strong upside momentum.

Market Sentiment and Outlook

- Despite the broader correction, market sentiment has recently turned firmer.

- Prices are showing early signs of stabilisation, supported by improving downstream demand and renewed export concerns from Indonesia, particularly around tighter export flows and policy uncertainty.

- While vegetable oil price correlations remain relevant, near-term fatty alcohol pricing is increasingly influenced by regional supply discipline and export dynamics.