-b_Big.jpg "China's Sulphuric Acid Export Ban Sparks Supply Chain Crisis")

Sulphuric Acid Global Market Disruption

The global sulphuric acid market is undergoing a structural disruption of significant magnitude, driven by a convergence of two independent but mutually reinforcing forces: China's unilateral restriction on sulphuric acid exports to protect domestic downstream industries, and ongoing geopolitical tensions in the Middle East that have severely curtailed sulphur supply flows through the Strait of Hormuz. The combined effect of these developments has triggered an unprecedented price surge across key consumption markets, with China's domestic price nearly doubling from $149 per metric tonne in the first week of March 2026 to $307 per metric tonne by mid-April 2026 a staggering increase of over 106 per cent in just six weeks.

India, another significant importer of Chinese sulphuric acid, has not been immune to these dynamics. Indian market prices have risen from a parallel low of $149 per metric tonne in early March 2026 to $278 per metric tonne by the second week of April 2026 an increase of approximately or above 87 per cent. These price movements are not transient; they signal a deeper structural realignment in global acid supply chains that may take months if not years to normalise.

Global Price Environment: A Dramatic Escalation

As in the first week of March 2026, sulphuric acid was transacting at $149 per metric tonne across both China's domestic market and India's import-linked pricing a figure broadly consistent with the historical range seen during periods of balanced supply-demand.

Within a span of approximately six weeks, prices have broken out aggressively from this equilibrium:

India's price, while relatively moderated, reflects a rapidly tightening import landscape as alternative supply origins become increasingly constrained.

China's Forthcoming Export Restriction: Rationale and Strategic Context

The Policy Decision: Export Restriction Effective May 2026

China has historically been the world's dominant exporter of sulphuric acid, leveraging its large-scale smelting and refining operations particularly in the copper, zinc, and lead smelting sectors where sulphuric acid is a by-product of sulphur dioxide (SO2) capture. This structural advantage gave China significant pricing leverage in global markets.

However, with the escalation of geopolitical tensions in the Persian Gulf region and consequent disruptions to sulphur imports via the Strait of Hormuz, China's own sulphuric acid production faces upstream raw material constraints. Recognising that domestic demand from the fertiliser sector, chemical processing industries, and metal leaching operations cannot be compromised, Chinese authorities and producers have moved decisively to prioritise the domestic market by curtailing export commitments.

This is not merely a commercial decision it carries strategic undertones. China's downstream industries, particularly phosphate-based fertilisers (which account for a substantial share of sulphuric acid consumption), are critical to food security and agricultural output. Any shortfall in sulphuric acid supply would cascade through the fertiliser production chain, with potentially severe implications for crop yields and food prices domestically.

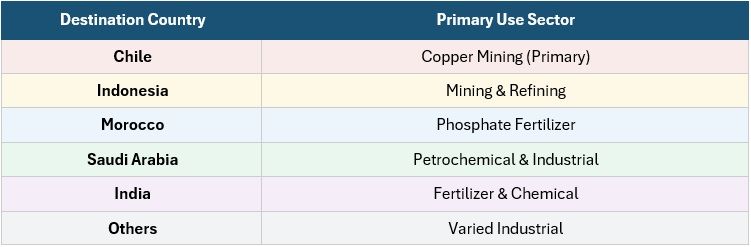

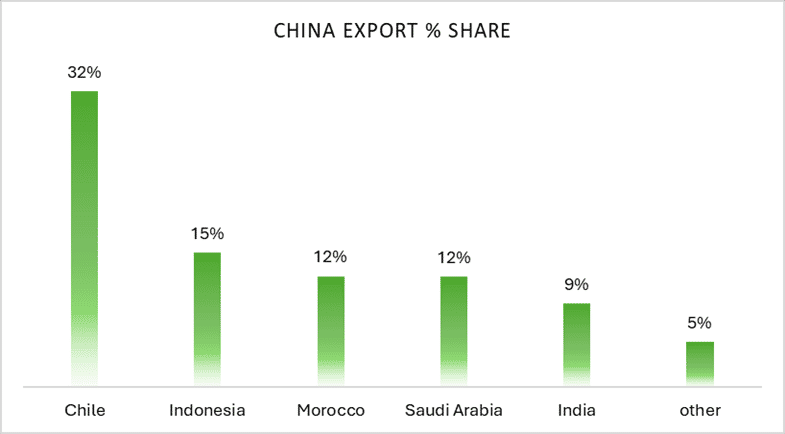

China's Export Destination Impact Assessment

China's sulphuric acid exports reach a diverse set of industries and geographies. The following table illustrates the export destination distribution and the sectors most at risk from China's supply withdrawal:

Chile, accounting for 32 per cent of China's sulphuric acid exports, faces the most acute exposure. The Chilean copper mining industry relies heavily on sulphuric acid for cheap leach operations used to extract copper from low-grade oxide ores. A reduction in Chinese supply would directly constrain copper output at a time when global copper demand remains robust, potentially introducing second-order disruptions across the industrial metals market.

Indonesia (15 per cent) faces disruptions to its mining and nickel refining sector. Morocco (12 per cent) is heavily exposed through its phosphate and fertiliser production. Saudi Arabia (12 per cent), though itself a petrochemical powerhouse, depends on Chinese acid for certain downstream chemical processes. India (9 per cent), as a major agricultural economy with significant fertiliser demand, confronts both a supply shortfall and a higher price burden simultaneously.

The Middle East Dimension: Strait of Hormuz and Sulphur Supply Risk

The Strait of Hormuz, the narrow maritime chokepoint between the Persian Gulf and the Gulf of Oman, is critical to the global sulphur trade. A significant portion of the world's elemental sulphur a key feedstock used to produce sulphuric acid via the contact process is sourced from refinery operations in Saudi Arabia, the UAE, Kuwait, and Qatar, and is shipped outward through this strait to markets in Asia, the America, and Africa.

The current geopolitical tensions in the region involving concerns over maritime security, potential naval confrontations, and the broader strategic standoff have introduced substantial freight risk and shipping uncertainty through this waterway. While physical flows have not entirely ceased, insurance premiums on tanker voyages through the Strait have surged and buyers have become cautious about forward procurement commitments relying on Persian Gulf supply.

For China, which receives a meaningful share of its sulphur from this region, this uncertainty directly threatens the raw material availability needed to sustain its sulphuric acid production, adding a further layer of urgency to its decision to restrict exports and secure domestic supply.

Downstream Industry Dependencies: Who Bears the Greatest Risk?

Sulphuric acid is one of the most versatile and widely consumed industrial chemicals in the world. Its criticality spans multiple verticals, meaning that supply disruptions reverberate well beyond the acid market itself:

Fertiliser Manufacturing

The production of phosphoric acid an essential ingredient in diammonium phosphate (DAP) and monoammonium phosphate (MAP) fertilisers is entirely dependent on sulphuric acid. Countries like Morocco, India, and parts of Southeast Asia that rely on Chinese acid imports are likely to experience either reduced fertiliser output or significantly elevated input costs, which will ultimately be borne by agricultural producers.

Copper and Base Metal Mining

Heap leaching of copper oxide ores is among the largest end-uses of sulphuric acid globally. Chile, as the world's largest copper producer, is immediately exposed. Reduced acid availability would not only curtail Chilean copper production but could affect global copper prices and, by extension, the broader industrial supply chain dependent on copper including electric vehicle manufacturing, power infrastructure, and electronics.

Chemical Processing and Refining

Sulphuric acid is a fundamental reagent in the production of a wide array of chemicals including titanium dioxide (TiO₂), hydrofluoric acid, alkylation in petroleum refining, and synthetic fibres. Any sustained supply constraint would create cost pressure and potential production bottlenecks across these allied industries.

Battery and Energy Storage Materials

Lead-acid batteries, though increasingly supplemented by lithium-ion technologies, still represent a significant volume market for sulphuric acid, particularly in developing markets. Additionally, hydrometallurgical processing of lithium and nickel key inputs to lithium-ion batteries employs sulphuric acid in leaching operations. Disruptions in acid supply could introduce unexpected bottlenecks in energy transition material supply chains.

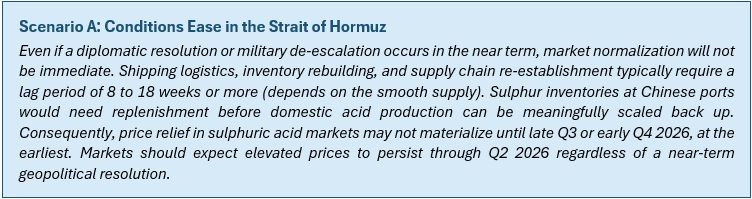

Scenario Analysis: Conditional Outlook

Scenario A — Geopolitical Easing

In this scenario, the following progression is anticipated:

- Sulphur flows resume gradually through the Strait over 4 to 8 weeks post-resolution

- Chinese domestic sulphuric acid production begins recovering, reducing urgency for export restrictions

- Export restrictions may be eased selectively, prioritising long-term trading partners

- Global acid prices progressively moderate from peak levels, though unlikely to revert to pre-March 2026 lows before Q4 2026

- Fertiliser and mining sector input costs remain elevated during the transition period

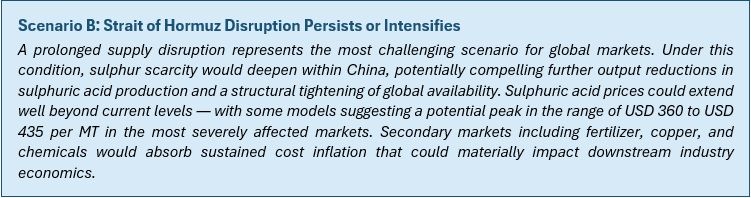

Scenario B Continued or Escalating Tension

In this scenario, the following consequences are plausible:

- Chinese sulphuric acid prices breach $350 per MT as sulphur inventories deplete

- Export restrictions become formalised through policy or force majeure declarations

- Chile, Morocco, and Indonesia are forced to source from alternative even from costlier origins.

- Indian fertiliser producers face dual pressure from both input cost escalation and potential domestic supply rationing

- Copper production disruptions in Chile add further inflationary pressure to industrial metals markets