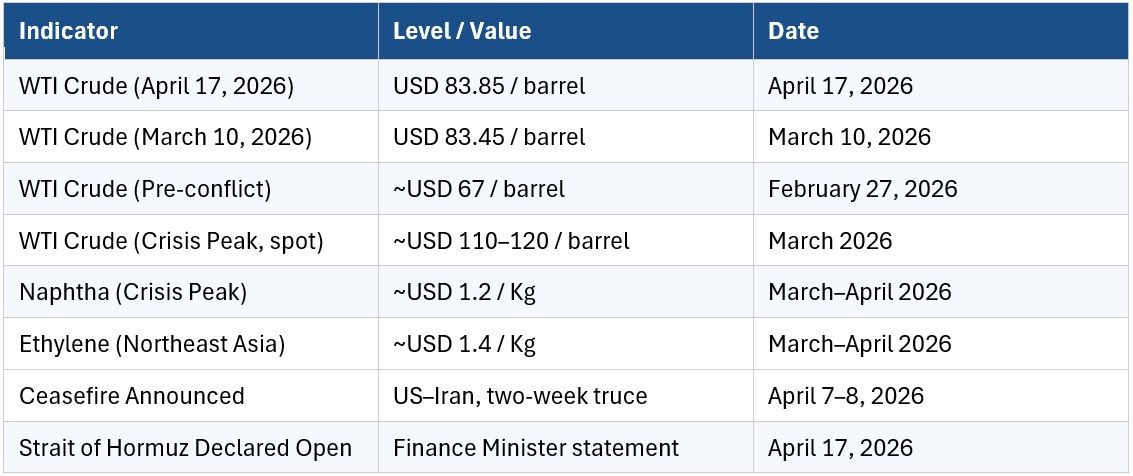

The global energy market witnessed one of its most turbulent swings in recent memory as West Texas Intermediate (WTI) crude oil the American benchmark closed at $83.85 per barrel on Friday, April 17, 2026. The significance of that number lies not just in its absolute value, but in what it represents: a return to territory last seen on March 10, 2026, when WTI had settled around $83.45, and a sharp unwinding of a crisis-premium that had been building for nearly seven weeks.

To understand the magnitude of this descent, one must look back to where crude was before the geopolitical storm gathered. On February 27, 2026, the eve of the US-Iran conflict and the subsequent blockade of the Strait of Hormuz WTI was trading near the $67 per barrel level. What followed was an unprecedented supply shock that drove crude to peaks near $110-120 per barrel on spot physical markets, representing an energy price emergency that has few historical comparators in peacetime.

The inflection point came on April 7, 2026, when the announcement of a fragile two-week ceasefire between the United States and Iran triggered an immediate and dramatic selloff. WTI registered one of its largest single-session percentage declines since April 2020. Then, on April 17, Iran’s Foreign Minister publicly declared the Strait of Hormuz fully open to commercial traffic during the truce period. The market reacted decisively WTI fell nearly 12 per cent in a single session to close at $83.85, completing an approximately 10-week round trip from pre-conflict levels back toward a post-crisis equilibrium.

Yet for the petrochemical industry, the road back to normalcy is far longer, far more complex, and far from guaranteed.

The Strait of Hormuz: Why One Chokepoint Paralysed the Global Chemical Supply Chain

The Strait of Hormuz is the jugular vein of the world’s energy system. Approximately 20 per cent of global crude oil supply and nearly 30 per cent of the world’s naphtha flows through this narrow maritime corridor between Iran and Oman. When Iran effectively blockaded the strait in late February and early March 2026, it did not merely create an oil shortage it surgically severed the feedstock lifeline of the global petrochemical industry.

The International Energy Agency (IEA), in its April 2026 Oil Market Report, quantified the devastation: global oil supply plummeted by 10.1 million barrels per day to 97 mb/d in March 2026, with OPEC+ production alone falling by 9.4 mb/d.

The consequence for the petrochemical sector was immediate and structural. As refineries in Asia scrambled for replacement feedstock and failed to find sufficient volumes naphtha, the primary building block of the Asian and European petrochemical complex, was no longer simply expensive. It had become scarce.

Naphtha at $1.200/Kg: The Crisis Behind the Crisis

While crude oil prices dominated headlines, the more significant impact for chemical manufacturers emerged within the naphtha market. Often referred to as the ‘primary feedstock’ of the petrochemical industry, naphtha prices surged to nearly $1.2 per Kg at the height of the crisis an increase of approximately 85 per cent compared to levels recorded just a month earlier.

As a key derivative of crude oil refining, naphtha pricing is closely tied to crude benchmarks. However, during the Hormuz disruption, this correlation intensified sharply. Supply constraints in Asia and Europe drove naphtha prices to levels that rendered conventional production economics unsustainable. Typically, naphtha accounts for around 65-75 per cent of total production costs in naphtha-based cracking operations; at $1.2 per kg, this cost structure became untenable.

Further downstream, ethylene the fundamental building block for polyethylene, PVC, polystyrene, and numerous other polymers experienced a sharp rise in Northeast Asian contract prices, reaching approximately $1.4 per kg. Despite this increase, product prices lagged the surge in feedstock costs, leading to significant compression in cracking margins across both Asian and European markets.

Downstream Impact: Ripple Effects Across End-Use Industries

The effects of feedstock disruption extended well beyond steam crackers, cascading through the broader petrochemical value chain and creating both cost inflation and supply constraints across multiple downstream sectors.

In plastics and packaging, key materials such as polyethylene and polypropylene experienced sharp price increases as reduced cracker output tightened supply. Converters supplying food packaging, consumer goods, and e-commerce industries faced higher raw material costs, along with allocation limits from resin producers in certain cases.

Within the automotive sector, reliance on materials like ABS plastics, polypropylene for interior applications, synthetic rubber, and coatings exposed supply chains to disruption. Shortages of critical intermediates led to extended lead times and increased cost pressures for OEMs (original equipment manufacturer) and their suppliers.

For construction materials, PVC widely used in pipes, window frames, and flooring came under pressure due to rising costs from both ethylene and chlorine inputs. This resulted in material cost escalation, particularly impacting infrastructure projects during sensitive execution phases.

In textiles and fibres, production of polyester and nylon primarily concentrated in Asia was constrained by limited availability of key intermediates such as PTA and caprolactam. These disruptions translated into higher costs for both apparel and technical textile applications.

Meanwhile, the agrochemicals and fertilisers segment also faced challenges, as several ammonia and urea producers in Asia were affected by disruptions in LNG flows through the Strait. Given that natural gas is the primary feedstock for nitrogen-based fertilisers, supply interruptions directly impacted production economics and availability.

Market Inflection Point: Petrochemical Outlook Following Crude Stabilisation

The correction in WTI crude prices to $83.85 has effectively removed the disruption-driven premium, marking a transition toward normalisation in petrochemical market dynamics. While this shift improves the cost environment for naphtha-based producers, the recovery path remains gradual and uneven.

Lower crude prices are structurally supportive, as they translate into reduced naphtha costs and create the potential for margin recovery, provided downstream pricing remains resilient. However, real market conditions suggest a lag between price signals and operational recovery.

Physical supply chains are still normalising, with delayed cargo movements expected to impact feedstock availability in Asia over the near term. At the same time, infrastructure constraints particularly in key LNG export hubs continue to limit energy supply, adding complexity to the recovery trajectory.

Inventory replenishment is another critical factor. Following significant stock drawdowns, especially across Asian markets, rebuilding to stable levels will require sustained inflows over the coming months, delaying full normalisation.

Geopolitical uncertainty also remains a key overhang. Ongoing negotiations between the United States and Iran continue to shape market sentiment, with unresolved differences likely to sustain a residual risk premium in energy markets.

Strategic Implications for the Petrochemical Sector

The events of February through April 2026 will reshape strategic planning across the petrochemical industry for years to come.

Feedstock diversification has moved from an aspiration to an operational imperative. BASF's newly inaugurated flex-feed cracker at its Zhanjiang Verbund site capable of switching between naphtha, butane, and other gas-based feedstocks provides the industry template. The ability to pivot between feedstock types is now a core competitive differentiator.

Supply chain regionalisation is accelerating. The crisis has validated local-for-local production models that reduce dependence on long-distance feedstock imports and geopolitically exposed maritime corridors.

The ethane-naphtha spread will be watched with renewed intensity as a leading indicator of regional competitiveness. US Gulf Coast producers are now firmly established as swing suppliers to global polymer markets during periods of Asian and European supply stress.

Working capital and inventory strategy will be fundamentally revisited. The speed and severity of the feedstock disruption caught many downstream manufacturers with insufficient buffer stock. Building more resilient inventory positions in critical polymers and intermediates will become standard practice.