Styrene monomer producers, the single largest downstream consumer of benzene are navigating their tightest feedstock cost environment in recent years. The pressure is flowing downstream to packaging, automotive, and consumer electronics supply chains, with benzene costs jumping sharply across Asian and European prices through Q1 2026, Styrene prices are stable from last one week after sliding ~5 per cent from the mid of April 2026.

Benzene's role as the foundational feedstock for the styrenics value chain ethylbenzene (EB), styrene monomer (SM), and ultimately polystyrene (PS), acrylonitrile butadiene styrene (ABS), and styrene-butadiene rubber (SBR) means that any sharp move in benzene spot prices reverberates immediately across a wide swath of the chemical and manufacturing industries. The EB/SM chain alone accounts for approximately 50 per cent of total global benzene consumption, making styrene monomer producers the most exposed downstream segment.

Styrene/Ethylene Current Prices

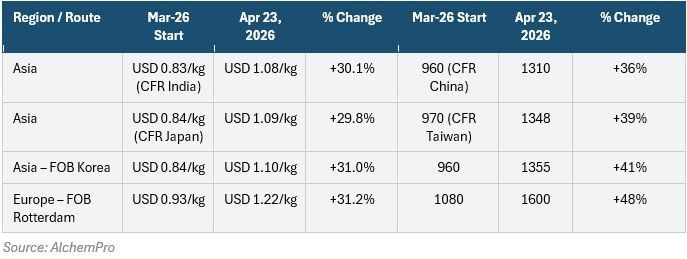

Asian prices

Styrene prices have risen faster than upstream costs, highlighting a strong link to benzene. While feedstocks (including ethylene) increased by about 30–31 per cent across Asia and Europe, styrene surged 39–48 per cent, reflecting additional pressure from benzene.

The key driver is a benzene price surge caused by higher raw material costs, which has pushed up styrene production costs more sharply. In Asia, Cost and Freight (CFR) China styrene rose from 960 to 1310 (+39 per cent), with similar increases in CFR Taiwan (+39 per cent) and Free on Board (FOB) Korea (+41 per cent). These gains exceed general feedstock inflation, indicating that costlier benzene has been the primary force lifting styrene prices, rather than ethylene alone.

European Prices

In Europe, market conditions are more pronounced. Benzene prices reached a record high of $1.27/kg on April 28, 2026, supported by pre-season restocking, constrained regional supply, and import parity from the Middle East. Producers of SM and PS are now facing significantly higher feedstock costs, adding to the burden of already elevated energy prices compared to 2025 levels. While seasonal demand from construction and coatings sectors is offering some support to volumes, margin recovery will largely depend on whether FOB Rotterdam benzene prices stabilise or continue to rise.

In Europe, the trend is even stronger. FOB Rotterdam styrene jumped 48 per cent (1081 to 1600), far above upstream cost increases (~31 per cent). This reflects a tighter and more expensive benzene market, amplifying cost pass-through into styrene.

Overall, styrene pricing is currently highly sensitive to benzene cost escalation, with rising raw material costs driving benzene higher—and in turn pushing styrene prices up disproportionately.

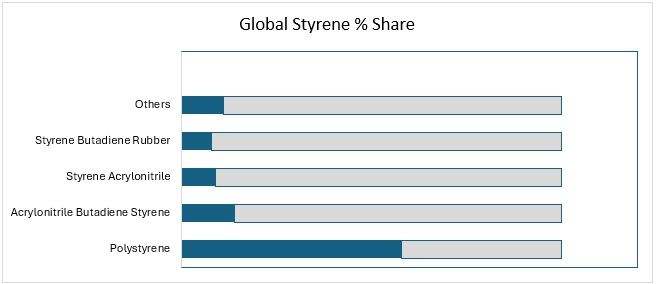

Styrene derivatives such as PS, ABS, and SBR are widely used in packaging, automotive parts, electronics, and construction materials. Their demand is closely tied to consumer goods, infrastructure activity, and industrial manufacturing trends.

Benzene serves as the foundational feedstock for a wide range of downstream petrochemical derivatives. The distribution of global benzene consumption across end-use sectors reflects the dominance of the styrenics chain, which alone accounts for over half of total demand.

Feedstock Costs

Styrene prices have been driven higher primarily by rising benzene costs, as benzene is the key feedstock in styrene production. The sharp increase in benzene has lifted the overall cost base, making it the main factor supporting styrene values, while any softening in benzene would directly weigh on styrene prices.

Downstream SM

Demand from PS and ABS, which together account for 65 per cent of styrene consumption, remains firm, supported by recovery in packaging, appliances, and construction-related sectors. Additional support comes from SBR latex demand and seasonal restocking.

Supply Tightness and Plant Outages

Unplanned downtime at several production facilities in Northeast Asia, particularly in South Korea and Japan, tightened domestic availability and intensified competition among downstream buyers through the observation period. Reduced import availability into India from Asian and Middle Eastern suppliers further supported spot price strength on CFR India assessments.

Arbitrage and International Trade Flows

South Korea is the world's largest benzene exporter. The widening Europe-Asia spread in late April 2026 is expected to redirect a portion of Korean export cargoes westward, potentially compressing the FOB Korea-FOB Rotterdam differential while tightening Asian spot availability.

Top Global Benzene Exporters (2024)

- US — $1.7 billion

- Saudi Arabia — $1.4 billion

- Netherlands — $1.3 billion

- Singapore — $530 billion

- Taiwan — $442 million

The short-term SM market is holding firm, supported by high feedstock costs, disciplined production in Northeast Asia, and an increasing divergence between European and Asian price trends.

Elevated crude oil continues to support benzene values across regions, while ethylene prices are rising more sharply in Europe, putting greater pressure on SM production margins there compared to Asia, where prices have shown early signs of stabilising. After a ~5 per cent correction in mid-April 2026, SM prices have largely stabilised, indicating the market is now aligned with feedstock cost levels rather than weakening demand.

On the demand side, purchasing activity from PS and ABS producers remains cautious, with buyers procuring on a need-based basis. However, pre-season EPS restocking in Europe is providing additional support, reinforcing upward momentum in regional SM prices beyond feedstock-driven factors alone.