Asian chemical markets are experiencing a severe supply shock in sulphur and methanol two foundational industrial commodities, triggered by the escalating US-Iran geopolitical standoff and related disruptions across the Strait of Hormuz. Middle East production facilities, which supply the bulk of Asia's sulphur and methanol imports, are operating at critically low utilisation rates, pushing prices to multi-month highs and squeezing downstream industries across fertilisers, agrochemicals, petrochemicals, and industrial manufacturing.

Sulphur prices in China have surged approximately 70-80 per cent from their February 2026 lows from ~$0.549 per kg to a peak of ~$0.938 per kg. Meanwhile, CFR methanol import prices across Asia remain severely depressed at $0.435-0.662 per kg due to a demand-supply imbalance caused by sharply curtailed Middle East output. The downstream industry outlook is mixed: upstream commodity holders’ benefit, while cost-intensive manufacturing sectors face significant margin compression.

Geopolitical Context: The Unsolved Mystery of US–Iran Tensions

The current supply crisis has its roots in the sustained and unresolved US–Iran standoff, which has created acute uncertainty over shipping and production across the Persian Gulf region. The Strait of Hormuz through which approximately 20 per cent of global oil and a significant share of petrochemical feedstock shipments pass has become the flashpoint for supply chain disruptions of a scale not seen in recent years.

The Strait of Hormuz remains the world's most critical maritime chokepoint for chemical commodities. Iran's posture of threatening to restrict or disrupt vessel movement through the Strait has created a persistent freight risk premium, forcing importers to seek alternative longer-haul supply routes adding significant cost and lead times. Insurance rates on shipments transiting the Gulf have escalated sharply, Persian Gulf petrochemical hubs including Iran, Saudi Arabia, Qatar, and UAE collectively supply over 50 per cent of China's sulphur import requirements and a dominant share of global methanol exports.

- Vessel owners are increasingly declining bookings through the Strait, with some major shipping lines rerouting

- The absence of a diplomatic breakthrough between US and Iran has left commodity markets in a state of prolonged structural uncertainty.

Russia Export Ban: A Compounding Factor

Adding to the supply pressure, Russia historically a significant exporter of sulphur, particularly as a by-product of its refining and natural gas processing operations has imposed export restrictions on Sulphur shipments. This ban, layered atop the Middle East disruption, has effectively eliminated two of the most significant global sulphur supply sources simultaneously, tightening the market to an extreme degree.

Russia's contribution to global sulphur trade, while secondary to Middle Eastern sources, had served as a partial buffer during past regional disruptions. The concurrent removal of this buffer has transformed a supply concern into a supply crisis, leaving Asia particularly China and India with severely constrained import options.

Sulphur Market: Price Surge & Supply Breakdown

China Sulphur Price Trajectory, US$ Per Kg (Converted from RMB)

Th market has experienced one of its sharpest upward re-ratings in recent weeks.

China Domestic Sulphur Price — February to April 2026

China's Import Dependence on Middle East Sulphur

China is the world's largest importer of sulphur, consuming it primarily for sulphuric acid production, which feeds the phosphate fertiliser and agrochemical industries. Critically, China sources over 50 per cent of its sulphur imports from Middle Eastern producers primarily Saudi Arabia (ARAMCO/SABIC), UAE, and Qatar. With these supply lanes now severely disrupted, China has been forced to seek spot cargoes from secondary markets at significant cost premiums, driving domestic prices sharply higher.

Methanol Market: Production Collapse & Price Dynamics

Middle East Methanol Production Crisis

The Middle East is home to some of the world's largest and most cost-competitive methanol production facilities, including major plants in Iran, Saudi Arabia, and Oman that collectively supply a dominant share of Asia's import needs. The current geopolitical environment has driven these facilities to drastically curtailed output levels, with production rates estimated at just 20-30 per cent of nameplate capacity, representing an effective output dip of 70-80 per cent or more from normalised run-rates.

Iranian methanol plants, including KIMIA Methanol, Kaveh Petrochemical, and Marjan Petrochemical were among the region's largest producers prior to the current crisis. Sanctions, shipping restrictions, and operational uncertainty have combined to effectively remove Iranian supply from the accessible global market.

Methanol CFR Import Prices Across Asia — As of April 27, 2026

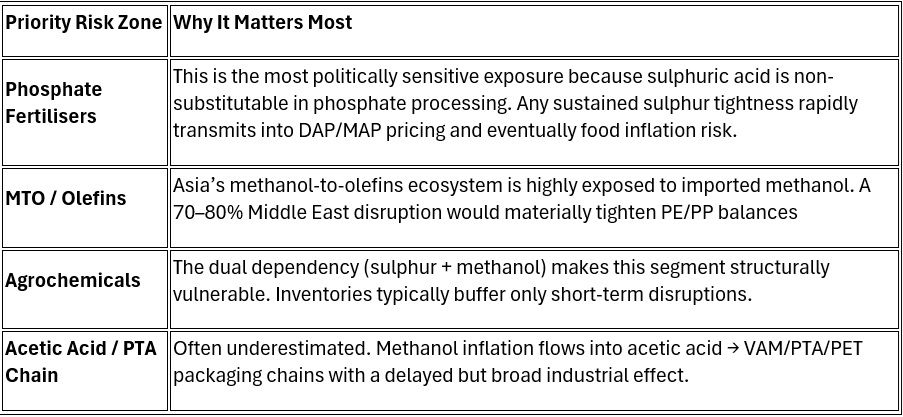

Downstream Industry Impact Assessment

Sectors Under Hard Pressure

Downstream Impact Heatmap, Industries Affected by Sulphur & Methanol Disruption