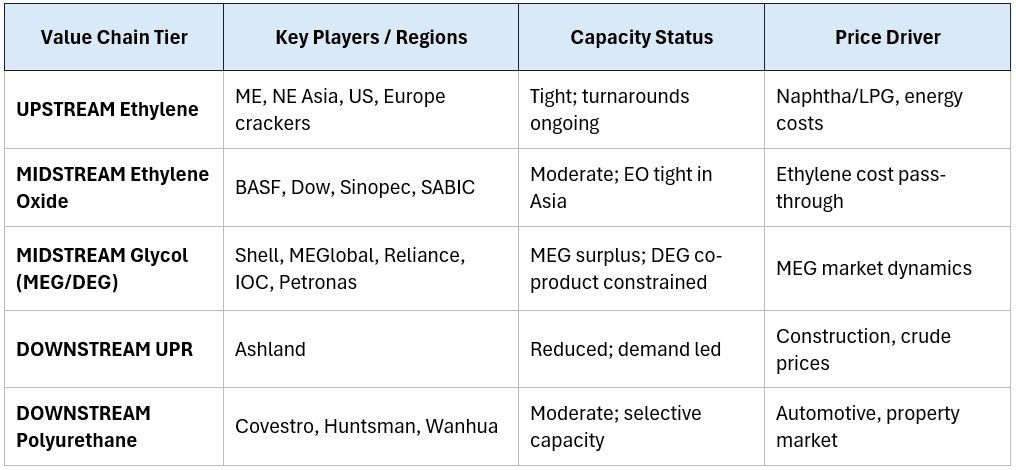

Diethylene glycol (DEG) markets across Asia entered a phase of sustained cost-driven inflation between March and May 2026, with prices in India (Kandla bulk) surging approximately 94 per cent from February lows to reach $0.892/kg by May 3, 2026. The corresponding China FOB export assessment rose ~93 per cent to $0.810/kg over the same period. Critically, this rally reflects upstream ethylene cost escalation and constrained glycol supply rather than genuine demand recovery a distinction with material implications for buyers and producers across the value chain.

Downstream consumption segments most notably Unsaturated Polyester Resins (UPR) and polyurethanes are operating at reduced utilisation rates, with procurement sentiment remaining defensively cautious. Elevated crude oil volatility, uncertain trade policy developments, and compressed processor margins have collectively suppressed discretionary buying, elongating procurement cycles and amplifying inventory destocking pressures.

DEG Price Trend Feb to May 2026

The Diethylene Glycol (DEG) market showed a steady upward trend from February to April, driven by firm feedstock ethylene costs, improved downstream demand from resins, polyester, and antifreeze industries, along with tighter regional supply conditions. Asia Domestic India (Kandla) bulk prices increased from approximately $0.46/kg in early February to nearly $0.89/kg by late April, reflecting an estimated rise of about 93.5 per cent, while Asia FOB China export prices rose from around $0.39/kg to $0.81/kg, indicating an increase of nearly 107.7 per cent.

The market sentiment remained cautious despite the bullish pricing trend, as geopolitical tensions and uncertainty surrounding a potential US-Iran peace agreement continued to influence crude oil and feedstock market direction. Most downstream buyers maintained a wait-and-watch approach and avoided aggressive bulk purchasing until clearer pricing stability emerged.

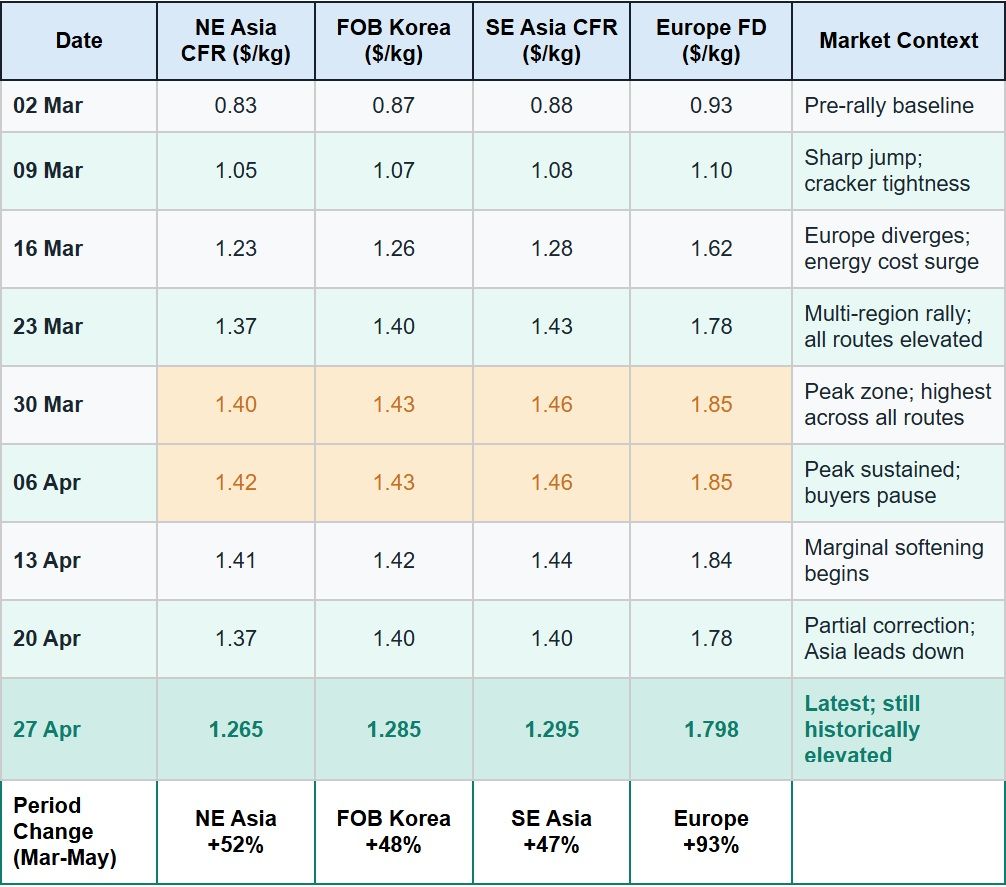

Ethylene prices across all major trade routes recorded sharp, broad-based increases from the first week of March 2026. The escalation was driven by a combination of unplanned cracker outages in Northeast Asia, elevated naphtha and LPG feedstock costs amid firming crude oil, and accelerating demand from downstream ethylene derivatives including MEG, vinyl acetate, and polyethylene. European values diverged most sharply reaching $1.798/kg FD amplified by natural gas price volatility and energy transition compliance costs affecting production economics.

Although prices remained historically high towards late April, slight corrections emerged as buyers resisted higher offers and adopted a cautious wait-and-watch approach amid geopolitical uncertainty and expectations surrounding a possible US-Iran peace deal, which could influence crude oil and feedstock market direction.

For DEG Buyers: Maintain short-cycle procurement (2-4-week horizons). Avoid spot over-coverage above $0.90/kg India. Monitor ethylene cracker turnaround schedules for Q3 2026 as leading indicator of supply relief.

For DEG Producers: Cost pass-through viability remains constrained by demand resistance. Evaluate MEG/DEG split optimisation. Prioritise markets with lower price elasticity (functional fluids, pharma-adjacent).

For UPR & PU Processors: Engage in structured dialogue with DEG suppliers for quarterly pricing arrangements. Model downside DEG scenarios into finished goods pricing to avoid margin lock-in at elevated input costs.

For Traders & Distributors: Position cautiously on inventory.