IPA Market Stabilises Amid Propylene Volatility and Iran Risks

The global Isopropyl Alcohol (IPA) market entered a phase of temporary stabilisation during the second week of May 2026 after experiencing a sharp correction in the opening week of the month. The market decline was primarily linked to weakness in upstream propylene oxide and propylene feedstock values, coupled with cautious downstream procurement activity across Asia. However, after first week of May, pricing sentiment stabilised as Chinese export offers for propylene oxide stopped declining after a significant correction of nearly $200/MT.

Isopropyl Alcohol (IPA) Markets are increasingly pricing in risks related to Iranian crude supply disruptions, Strait of Hormuz security concerns, and tighter sanctions, which continue to impact upstream propylene and propylene oxide markets linked to Isopropyl Alcohol (IPA) production. Any further geopolitical escalation could trigger another round of feedstock-driven IPA price increases across solvents, pharmaceuticals, coatings, and electronics sectors.

Potential talks between Donald Trump and Xi Jinping may provide some relief to crude oil and petrochemical markets, as China remains the largest importer of Middle Eastern crude oil. However, IPA market sentiment remains cautious amid ongoing US-Iran tensions and crude oil volatility.

The global Isopropyl Alcohol (IPA) market witnessed a strong upward trend from early March to mid-April 2026, followed by a correction phase and subsequent stabilisation over the last week. Asia Domestic India (Kandla) bulk IPA prices increased from around $0.90/kg in late February to a peak near $2.00/kg during April, reflecting a sharp rise of more than 120 per cent during the rally period. Similarly, Europe FOB Rotterdam export prices climbed from nearly $1.35/kg to around $1.80/kg, marking an increase of approximately 33 per cent, while Asia FOB China export prices rose from nearly $0.72/kg to around $1.13/kg, up by nearly 57 per cent. USA FOB US Gulf export prices also strengthened from approximately $0.80/kg to $0.94/kg, recording a comparatively moderate gain of around 18 per cent.

However, after mid-April, the market entered a correction phase driven by weaker downstream buying interest, easing feedstock pressure, and cautious sentiment across solvent markets. During the latest trading week, IPA prices across major regions remained largely stable with only marginal fluctuations, indicating that the market has temporarily reached equilibrium after the earlier volatility. Stable propylene oxide pricing in China following the nearly $200/MT correction, combined with cautious downstream procurement activity, has contributed to the current range-bound trend. Market participants are now waiting for clearer direction from upstream crude oil and propylene markets before initiating aggressive buying or pricing revisions.

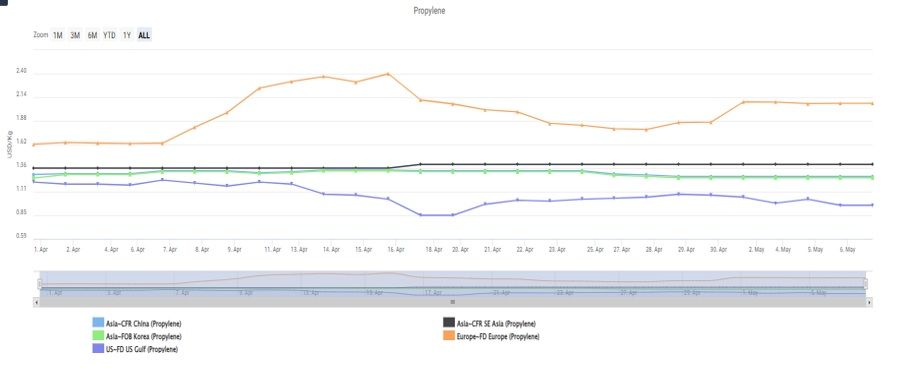

The upstream propylene market, a key feedstock driver for Isopropyl Alcohol (IPA), displayed mixed regional pricing trends during April to early May 2026, significantly influencing overall IPA market sentiment. Europe FD Europe propylene prices recorded the strongest volatility, rising sharply from nearly $1.60/kg in early April to a peak close to $2.40/kg by mid-April, reflecting an increase of almost 50 per cent before easing slightly toward early May. The strong European rally was largely supported by higher crude oil-linked feedstock costs and tighter regional supply conditions.

In Asia, CFR Southeast Asia propylene prices remained comparatively stable, moving within the $1.30-1.36/kg range throughout the review period, indicating balanced supply-demand fundamentals. FOB Korea propylene prices also remained relatively flat near $1.25-1.30/kg with only marginal fluctuations. Meanwhile, CFR China propylene prices showed a weaker trend, declining from around $1.20/kg in early April to below $0.90/kg by mid-to-late April before stabilising near $0.95/kg in early May. USA FOB US Gulf propylene prices similarly softened during April, reflecting weaker downstream demand and cautious buying activity.

The correction and subsequent stabilisation in Chinese propylene prices directly impacted the IPA market, particularly across Asia, as propylene remains one of the primary feedstocks for IPA production. The sharp decline in upstream propylene and propylene oxide values during April reduced production cost pressure for IPA manufacturers, contributing to the recent stabilisation observed in IPA prices after the earlier correction phase. However, continued volatility in global crude oil markets is keeping upstream propylene markets uncertain, causing both IPA producers and downstream buyers to remain cautious. As a result, the IPA market is currently moving in a stable-to-range-bound pattern, closely tracking feedstock direction and downstream demand recovery signals.

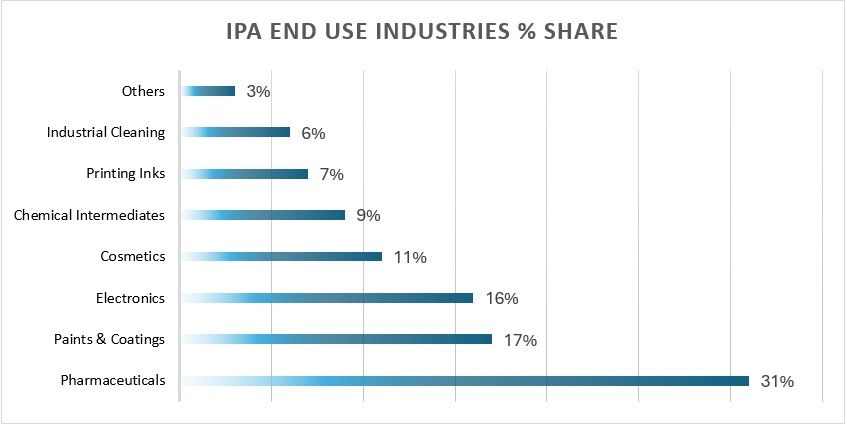

On the downstream side, major IPA-consuming industries including pharmaceuticals, paints & coatings, electronics, printing inks, cosmetics, disinfectants, and industrial cleaning sectors are largely purchasing on a need-based basis. Buyers remain cautious due to uncertain end-user demand recovery and fluctuating raw material costs. Many downstream consumers are delaying large-volume procurement decisions while waiting for better visibility on demand trends, export activity, and crude-linked feedstock stability. This restrained purchasing behaviour has prevented a sharp rebound in IPA prices despite stabilisation in upstream raw materials.

IPA pricing behaviour indicates that the market is transitioning from a correction phase into a stabilisation phase. The absence of aggressive spot buying suggests that downstream industries are still uncertain about near-term demand recovery. Meanwhile, crude oil volatility and the highly fluctuating geopolitical situation continue to limit visibility for upstream propylene pricing, as ongoing tensions in key oil-producing regions are contributing to unpredictable energy markets, supply chain disruptions, and sudden feedstock cost fluctuations. Unless a significant improvement in downstream industrial demand emerges, IPA prices are expected to remain within a narrow trading range over the short term. However, any sharp rebound in crude oil or propylene markets—potentially triggered by escalating geopolitical risks, production cuts, or supply disruptions—could quickly reintroduce upward pressure across the IPA value chain.