Global toluene diisocyanate (TDI) markets entered May 2026 under intensifying pressure, with prices correcting sharply after the first week of the month. A confluence of limited downstream demand, elevated raw material costs, softening crude oil in first week of May 2026, and the emergence of US–Iran peace negotiations triggered a sentiment-driven dip of approximately 6-8 per cent of TDI prices. Moreover, TDI prices remained largely stable despite the surge in crude oil prices during the second week of May, as feedstock toluene to trend on the upper stable side.

Prices have since stabilised at lower levels as buyers remain cautious and sellers resist further discounting amid persistently high production costs. The price correction has significantly compressed the TDI–Toluene spread, squeezing producer margins and reducing export competitiveness from China.

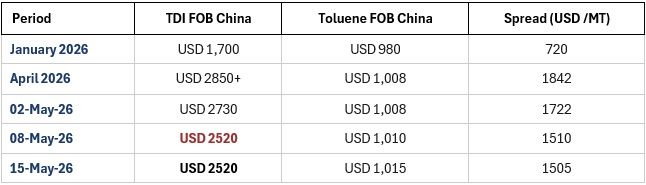

Global TDI prices exhibited mixed but predominantly firm trends during May 2026 across major trade routes. Free on Board (FOB) China prices increased sharply from $1,700/MT in January 2026 to $2,730/MT on May 02, reflecting a rise of nearly 60.6 per cent. However, prices corrected thereafter and stabilised at $2,520/MT by both May 08 and May 15, representing a decline of around 7.7 per cent from early May levels while remaining 48.2 per cent higher compared to January. Similarly, Cost, Insurance and Freight (CIF) Europe prices rose from $2,165/MT in January to $2,895/MT on May 02, an increase of approximately 33.7 per cent, before easing to $2,610/MT by mid-May, marking a correction of 9.8 per cent from the May peak.

In other Asian markets, CIF South Korea prices climbed from $1,850/MT in January to $2,720/MT on May 02, registering a strong increase of nearly 47.0 per cent, before moderating to $2,570/MT by May 15, down 5.5 per cent from the peak level. Meanwhile, CIF Southeast Asia displayed the strongest overall gains, rising from $1,773/MT in January to $2,780/MT on May 02 and further strengthening to $2,920/MT by mid-May. This represented a substantial increase of nearly 64.7 per cent compared to January levels. Overall, the global TDI market continued to witness elevated pricing compared to the beginning of the year, despite partial corrections observed after the first week of May.

Toluene: Raw Material Correlation and Pricing

Toluene is the primary aromatic feedstock for TDI manufacturing, accounting for approximately 55–60 per cent of variable production costs. Its price behaviour has a direct and material influence on TDI production economics. The May 2026 dynamic reveals a critical asymmetry: while TDI prices dropped 6-8 per cent on sentiment and demand weakness, toluene prices in Asia remained firm or edged higher intensifying the margin pressure on TDI producers.

Global toluene markets displayed mixed pricing trends during the second week of May 2026. Asian export markets witnessed moderate gains, with FOB China prices increasing by 0.69 per cent and FOB South Korea rising by 1.47 per cent, supported by firmer regional demand and improving sentiment. The US Gulf market also strengthened marginally, while Rotterdam prices edged slightly lower amid softer European buying activity. Meanwhile, import prices across India and Southeast Asia remained relatively stable, indicating balanced regional supply conditions despite fluctuations in upstream crude oil markets.

Subdued Downstream Demand

Flexible foam, coatings, adhesives, furniture, and bedding sectors continued to display restrained procurement activity during May 2026. Buyers largely preferred to reduce existing inventories instead of entering fresh contracts at elevated price levels, resulting in weaker spot market participation and softer overall TDI demand sentiment.

Crude Oil Softness Expectation

Expectations surrounding a potential US–Iran peace agreement triggered a notable decline in crude oil prices during early May 2026. The weakening energy complex directly impacted petrochemical sentiment, leading to a broad correction across TDI markets.

Elevated Raw Material Costs

Despite the sharp correction in TDI prices, upstream feedstock costs remained relatively firm. Asian toluene prices continued to hold within the range of $1,008–$1,038/MT, providing a cost-support mechanism for producers and preventing a deeper decline in TDI prices.

Geopolitical Normalisation

The improving geopolitical environment and easing tensions between the US and Iran reduced the macro risk premium embedded in global energy markets. This encouraged buyers to postpone procurement activity in anticipation of further crude-linked price declines, thereby amplifying short-term demand weakness in the TDI market.

Chinese Export Competition

Chinese producers maintained highly competitive FOB export offers at around $2500/MT in an effort to clear surplus inventories amid sluggish domestic demand. The aggressive export pricing widened the spread against European benchmarks by more than $400/MT, increasing pressure on regional and global TDI trade flows.

Supply-Side Price Floor

Although demand conditions remained weak, high fixed production costs and compressed operating margins limited producers’ willingness to offer further discounts. Growing resistance from suppliers contributed to price stabilisation following the recent correction and helped establish a natural floor for global TDI prices.

The spread between TDI and its feedstock (toluene) is the most reliable indicator of producer profitability.

Market Outlook: Near-term View

TDI prices are expected to consolidate in the $2420/MT–$2600/MT FOB China range through the second half of May 2026, toluene feedstock remains relatively stable. The key question is whether the US–Iran geopolitical development materialises into a sustained crude oil correction or proves to be a temporary sentiment-led move.

Key indicators to monitor:

- Toluene FOB China spot direction, a sustained move above $1,050/MT would underpin a TDI price floor.

- Brent crude oil trajectory, further weakness below $80/barrel could extend the TDI correction to 13–15 per cent from May opening levels.

- Downstream demand signals furniture, bedding, and automotive foam order books for Q2 and Q3 2026.

- Chinese producer operating rates any capacity curtailments would tighten supply and support pricing.

- US–Iran diplomatic outcome a formal agreement would reinforce bearish crude sentiment; a breakdown could reverse it sharply.