Spike; Partial Relief in May 2026")

The global ethylene oxide (EO) market entered 2026 on a cautious recovery path, with prices gradually firming across all major regions after years of margin compression. That trajectory was violently interrupted on February 28, 2026, when armed conflict between Iran and Israel escalated into a full-scale confrontation one that has since become the most consequential supply disruption in the history of the global petrochemical industry.

Prior to the conflict's escalation, the EO market was displaying a familiar pattern of cautious recovery. Feedstock ethylene costs had been edging higher on the back of gradually firming crude oil prices, while downstream demand from textile, healthcare, and personal care sectors was picking up moderately after a prolonged period of inventory correction.

China Partial Correction from War-Peak; Import Dependency Persists

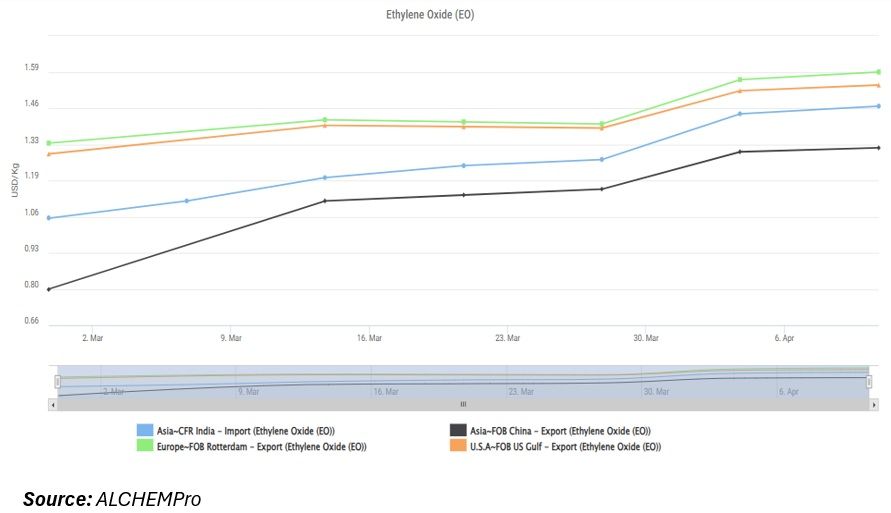

China's EO market was the epicentre of the war-driven price shock. FOB prices climbed from approximately $0.796 per kg at the end of February 2026 to around $1.313 per kg by April 10 a 65 per cent increase in six weeks that had no parallel in the modern EO market. The speed and magnitude of the move reflected two concurrent dynamics: the broad global supply shock from Hormuz closure, and China's specific structural dependence on Middle Eastern petrochemical intermediates that flow through complex indirect trading routes given existing trade restrictions.

By May 1, prices had partially settled at $1.32 per kg still well above pre-war levels but below the April peak. The May 6 step-down to $1.21 per kg a reduction of $0.11 per kg (−8.3 per cent) in a single day reflects a concurrent softening in Asian ethylene feedstock costs (CFR China ethylene: $1,100per t, flat). The $0.11 per kg May correction is modest relative to the $0.517 per kg war-surge, signalling that the China EO market remains in structurally elevated territory, not yet returning towards pre-war norms.

Key downstream exposed sectors (China): Textile and polyester fibre manufacturers (EO → MEG → PET), surfactant producers for personal care exports, and industrial ethylene glycol users for automotive antifreeze and heat exchangers.

India Structural Import Vulnerability; Freight Premium Persists

India's EO market has experienced the largest intra-May correction in dollar terms: a drop of $0.22 per kg (−13.4 per cent) from $1.64 per kg on May 1 to $1.42 per kg from May 6 onward. This correction is significant but must be contextualised: CFR India prices include a freight, insurance, and logistics premium that makes the landed cost structurally higher than FOB benchmarks. Even at $1.42 per kg, India's EO import cost remains approximately 17 per cent above Chinese FOB a spread that reflects real import-cost economics rather than demand premium.

India's pharmaceutical sector is the most strategically exposed downstream user. EO is the sole approved sterilisation agent for a large category of single-use medical devices and surgical instruments, making it a critical input with no viable substitute. Supply disruption in this channel carries implications that extend well beyond chemical market economics into healthcare system reliability. At the same time, India's cosmetics and personal care sector, which uses EO-derived ethoxylates and surfactants, is absorbing the higher cost environment through selling price increases and formulation adjustments.

Northwest Europe High Base, Structural Naphtha Linkage

European EO prices have held the highest global benchmark level throughout the conflict period and remain the highest as of May 18 at $1.64 per kg FOB Rotterdam despite the May 6 correction of −$0.17 per kg. The European price premium is structural and persistent: naphtha-based ethylene production means that European EO costs move directly with global crude oil benchmarks, and crude remains elevated at $111.50 per bbl (Brent) as of May 18, 2026.

The May 6 softening in European EO corresponds to the mild decline in CIF Northwest Europe ethylene (−$ 5per t to $1,474per t) and a partial easing of Hormuz-related freight surcharges as Cape-rerouted vessel capacity slowly increased. However, with Brent crude still above $111 and the Barakah nuclear plant incident (May 17) introducing renewed upside risk, the structural floor for European EO is unlikely to soften materially in the near term. The risk for European buyers is that current elevated price levels become the new normal rather than a temporary crisis peak.

United States - Ethane Advantage Creates Structural Outperformance

The United States is the most distinctive market in the global EO comparison. While FOB US Gulf EO prices did rise during the April war peak (from ~$1.29 per kg to ~$1.54 per kg), the May 2026 price of $1.74-1.76 per kg represents a significant upward shift from those levels, reflecting not a new crisis premium but a realignment of the US price towards export-arbitrage-supported levels as global buyers compete for US-origin supply.

American EO producers use ethane, a natural gas liquid as their primary ethylene feedstock, insulating them almost entirely from the naphtha-crude oil cost escalation driving prices higher in Asia and Europe. This feedstock advantage has widened to its largest margin in over a decade. With Middle Eastern and Asian supply contracted, US-origin EO and ethylene derivatives have become premium-priced alternative supply sources globally. The mild May 12 price uptick to $1.76 per kg reflects continued export demand pull from Asia and Europe, supporting marginal upward pricing despite overall global market easing.

For EO Buyers / Downstream Converters

- EO prices remain elevated despite correction: Asia ($1.21–1.42 per kg), Europe ($1.64 per kg), US ($1.76 per kg), with limited downside unless geopolitical conditions improve.

- Maintain 30–45 days forward EO coverage to reduce exposure to potential June price volatility and bullish market risk.

- Increase sourcing diversification, especially US-origin EO, to reduce dependence on Middle Eastern supply chains.

- Track CFR Asia ethylene closely; levels above $1,300 per could trigger immediate EO repricing.