-b_Big.jpg "PFAD Prices Ease After March Peak Despite Ongoing US–Iran Conflict")

Palm Fatty Acid Distillate (PFAD) is a by-product obtained during the refining of crude palm oil. It appears as a brownish-yellow semi-solid material and turns into a thick liquid at temperatures above 40–45°C. PFAD mainly consists of free fatty acids, particularly palmitic and oleic acids, along with smaller amounts of linoleic and stearic acids. Owing to its high fatty acid content, PFAD is widely used as a raw material in soap manufacturing, biodiesel production, lubricants, and the oleochemical industry for producing fatty acids, fatty alcohols, and methyl esters.

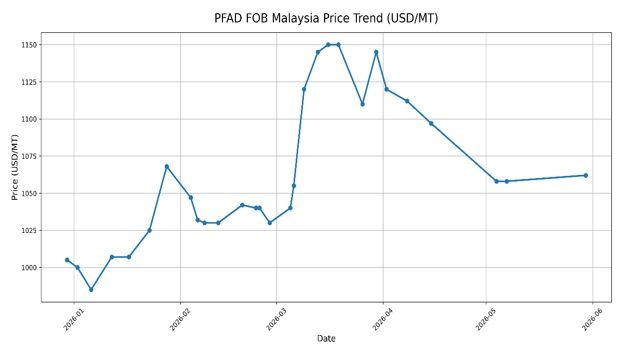

The PFAD price story across May 2025 to May 2026 is one of significant recovery and renewed bullish momentum. From a sharp trough of approximately $843 per MT Free on Board (FOB) Malaysia in June 2025, prices have climbed steadily and consistently to reach $1,055 per MT FOB Malaysia as of May 15 2026 a recovery of approximately 26 per cent from the mid-year low.

The stronger upward movement observed during March–April 2026 was further supported by rising geopolitical tensions between the US and Iran, which increased crude oil prices and strengthened biodiesel market sentiment. Since PFAD is widely used as a biofuel feedstock, higher energy prices and concerns over global supply disruptions contributed to additional bullish momentum in PFAD markets.

The CY 2025 began on a firm footing at $990 per MT FOB Malaysia, briefly rallied to ~$1,025 per MT in March 2025, before succumbing to the seasonal mid-year correction (June–July) that is characteristic of the palm complex during high production seasons in Malaysia and Indonesia. The June 2025 through coincided with peak Q3 crop arrivals from Sabah and Sarawak, combined with subdued downstream buying amid high port inventory levels across South Asian and Chinese import terminals.

The recovery phase (August–December 2025) was robust and methodical. By September 2025, PFAD FOB Malaysia had recovered to ~$970 per MT, and by December 2025 it had crossed the $990–$1,005 per MT range, setting the stage for a strong entry into 2026.

The December 2025–May 2026 price series, compiled from market intelligence, shows a far more granular picture. PFAD FOB Malaysia traded in a tight$985–$1,000 per MT range in the first week of January 2026, then staged a decisive rally through February and into March 2026. By mid-March 2026, PFAD prices had surged to nearly $1,150 per MT FOB Malaysia, largely driven by escalating US–Iran geopolitical tensions and the resulting rise in global crude oil prices. Concerns over possible disruptions in key oil shipping routes, particularly around the Strait of Hormuz, increased volatility across global energy and vegetable oil markets. The sharp increase in crude oil values improved biodiesel competitiveness and strengthened speculative buying interest across the palm complex, which contributed significantly to the rally in PFAD prices during the period.

However, by April 2026 prices softened from the March highs, correcting to ~$1,110–$1,120 per MT in the first week of April. The May 2026 price ($1,060 per MT as of May 15) represents a further consolidation, down approximately 4.5 per cent from the March peak but still commanding a strong 16 per cent premium over the same period last year (May 2025: $915 per MT FOB Malaysia).

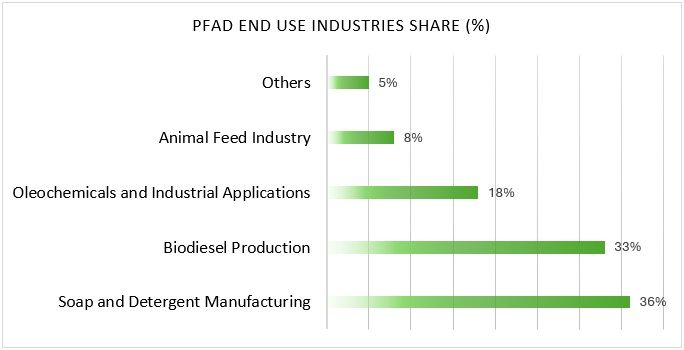

PFAD Consumption by End-Use Industry

Soap and detergent manufacturing remain the largest end-use sector for PFAD, accounting for 36 per cent of total consumption, followed closely by biodiesel production at 33 per cent. Industrial oleochemicals, animal feed, and other specialty applications collectively contribute the remaining market share, highlighting PFAD’s diversified industrial importance.

Indonesia Biodiesel Policy and PFAD Market Impact

Indonesia’s biodiesel policy remained a major driver of PFAD and broader palm oil market sentiment during 2025–2026. After implementing the B40 mandate in January 2025, Indonesia initially planned to increase blending requirements to B50 by mid-2026 as part of its strategy to reduce dependence on imported fossil fuels and minimise the economic impact of the ongoing US–Iran conflict and global energy market volatility. Expectations surrounding the proposed B50 rollout provided strong bullish support to crude palm oil and PFAD prices throughout late 2025 and early 2026, particularly during the March–April rally.

The Indonesian government introduced additional economic measures to protect domestic stability amid continuing global uncertainty and geopolitical tensions. President Prabowo Subianto’s administration announced new export proceeds (DHE) policies and tighter management of strategic commodity exports, including crude palm oil (CPO), to strengthen foreign exchange reserves and maintain economic resilience during the ongoing global conflict situation. These policies reinforced expectations of stronger domestic control over palm oil supplies and supported bullish sentiment across the palm and PFAD markets.

However, in early 2026, Indonesia postponed the B50 implementation, citing refinery infrastructure limitations, inadequate feedstock availability, and financial pressure on the palm oil export levy system. Despite the delay, the continuation of the B40 mandate still diverted substantial palm oil volumes toward domestic biodiesel production, thereby limiting PFAD export availability and continuing to support market prices.