-b_Big.jpg "Global Phenol Prices Ease from Peak but Stay Firm Week-on-Week")

The global phenol market has experienced one of its most volatile quarters in recent history. Prices surged sharply from early March 2026 following the outbreak of the US-Iran conflict and the effective closure of the Strait of Hormuz on February 28, 2026, disrupting global oil, LNG, and petrochemical feedstock flows. The phenol supply chain absorbed the largest upstream cost driving prices up by +49 per cent to +80 per cent across regions from early February to the April peak. Since the late April high, a modest correction has emerged most notably in global -4 per cent-9 per cent, primarily driven by weak demand in the European automotive and construction sectors and cautious buying strategies. North America remains the firmest market.

Week-on-Week Country-wise Phenol Price Trend

The global phenol market displayed significant volatility during the observed period, with prices across major regions witnessing strong gains from February through April before showing mixed week-on-week corrections in May. Supply tightness, elevated feedstock benzene costs, logistical disruptions, and improving downstream demand from the bisphenol-A and resins sectors largely supported the bullish market sentiment during the initial phase of the trend.

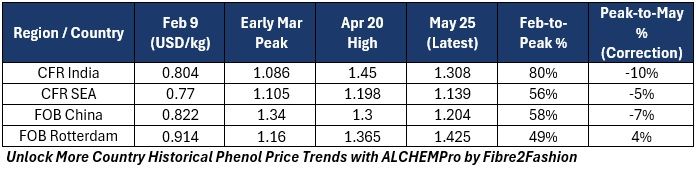

Among all regions, Cost and Freight (CFR) India recorded the sharpest rise in prices, increasing from $804/MT on February 9 to a peak of $1450/MT on April 20, reflecting an overall gain of 80.35 per cent. However, after reaching peak levels, prices corrected by 9.79 per cent by late May as buyers resisted higher offers and import activity slowed.

Similarly, CFR Southeast Asia prices increased by 55.58 per cent from February to peak levels amid constrained regional supply and firm import demand. Prices later declined by 4.92 per cent, indicating weaker weekly trading activity.

Free on Board (FOB) China prices also followed an upward trajectory, rising by 58.15 per cent between February and April due to production constraints and stronger export inquiries. Nevertheless, the Chinese market witnessed a 7.38 per cent correction after the peak, primarily influenced by easing domestic demand and improving inventory levels on a week-on-week basis.

In contrast, FOB Rotterdam maintained comparatively stronger stability. European phenol prices rose by 49.34 per cent from February levels and continued to gain an additional 4.40 per cent even after the April peak. Persistent supply limitations, higher production costs, and stable downstream consumption supported the firm weekly trend in the European market.

Overall, the market transitioned from aggressive bullishness toward a more balanced phase by May, with regional corrections emerging amid easing supply concerns and demand resistance.

The most decisive price catalyst in the review period was the outbreak of the US-Iran military conflict on February 28, 2026, and the subsequent disruption to shipping through the Strait of Hormuz, the world's most critical energy and petrochemical corridor:

Crude Oil Disruptions: OPEC+ production cuts, ongoing geopolitical tensions, tanker congestion, and rising war-risk insurance premiums pushed global crude oil benchmarks higher, resulting in increased production costs for benzene and propylene derivatives used in phenol manufacturing.

Benzene and Phenol Price Surge: Benzene prices strengthened significantly during the period, directly increasing cumene production costs under the Hock process route. Consequently, FOB China phenol prices climbed from around $822/MT in February to nearly $1,300/MT by April 2025, reflecting an increase of approximately 58 per cent within a short span amid tight regional supply conditions.

Freight and Insurance Costs: Escalating geopolitical risks in key shipping routes led to higher freight charges and war-risk insurance premiums for chemical cargoes. Increased transportation costs for benzene, cumene, and phenol shipments significantly raised landed import prices across Asian and European markets while limiting arbitrage opportunities.

Production Outages and Plant Maintenance: Planned maintenance turnarounds and unexpected shutdowns at several phenol production facilities in Asia, particularly in Japan and South Korea, tightened spot market availability. Reduced operating rates during a period of firm downstream demand intensified supply pressure across the regional market.

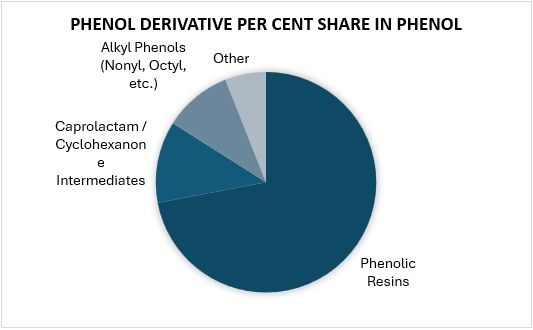

Restocking Demand from Downstream Industries: After a cautious procurement phase earlier in the year, downstream sectors including BPA, epoxy resins, and phenolic resins resumed active inventory replenishment. Stronger buying activity during the quarter further supported the upward momentum in phenol prices amid already constrained supply conditions.

Feedstock Cost Analysis: Benzene → Cumene → Phenol Chain

Phenol is produced almost exclusively via the cumene hydroperoxide (Hock) process, creating a direct cost-transmission chain from crude oil through benzene and propylene into phenol pricing.

Benzene (Primary Feedstock): Northeast (NE) Asian benzene surged sharply on the back of Middle East supply disruptions and refinery feedstock tightness.

Propylene: Propylene contract prices increased in both April and May 2026, squeezing cumene route economics and placing upward pressure on phenol-acetone margin stacks.

Crude Oil Linkage: The US-Iran conflict and Strait of Hormuz disruption created direct crude oil price spikes, sustaining elevated naphtha-reformate-benzene feedstock costs through Q1 and into Q2 2026.