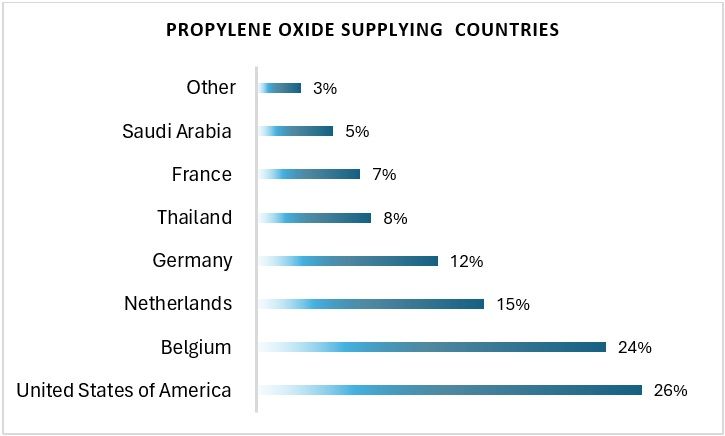

Propylene Oxide: A Sharp Reversal

Propylene Oxide prices in China staged a dramatic but short-lived rally through the first quarter and into early April 2026, surging from approximately $1,130 per MT in early March to a multi-month high near $1,823 per MT by mid-April. The entire gain has since been reversed, with the FOB China export price touching $1,391 per MT as of May 21 essentially retracing to where the market stood at the start of Q1.

Downstream producers are procuring strictly on requirement, the era of build-ahead inventory has given way to hand-to-mouth buying amid bearish sentiment and ample spot availability.

The price trend for Propylene Oxide (PO) in Asia FOB China showed significant fluctuations between early March and mid-May 2026. Prices started at approximately $1,130 per MT in early March and increased sharply to around $1,450 per MT by March 9, reflecting a rise of nearly 29.5 per cent. This strong upward movement was mainly driven by improved downstream demand, tighter supply availability, and higher feedstock propylene costs.

From mid-March to early April, the market continued its bullish momentum. Prices moved from about $1,450 per MT to a peak of nearly $1,820 per MT around April 6, representing an additional increase of approximately 25.5 per cent. The rise during this period was likely supported by firm industrial demand from polyurethane and chemical manufacturing sectors, along with supply-side constraints in the regional market.

After reaching the peak in early April, the PO market entered a downward correction phase. Prices gradually declined from $1,820 per MT to around $1,390 per MT by May 21, 2026, showing a decrease of approximately 23.6 per cent. The downward trend was mainly driven by improved supply availability, weaker purchasing activity, balanced inventory levels, and declining raw material costs. Weak export demand and cautious purchasing behaviour from downstream industries may also have contributed to the bearish trend.

Overall, despite the late-April and May correction, the market remained higher compared to the beginning of March. On a net basis, PO prices increased from approximately $1,120 per MT to $1,392 per MT, indicating an overall gain of around 24.3 per cent during the entire observed period.

Feedstock propylene prices have declined considerably, reducing the production cost pressure that previously supported the price surge seen during March and April. Meanwhile, demand conditions weakened as downstream industries such as polyurethane foam, propylene glycol, and surfactant manufacturing adopted a cautious purchasing approach, postponing new orders amid comfortable inventory positions and ongoing market uncertainty.

Downstream Industry Mapping: Where Demand Has Stalled

Propylene oxide feeds a diverse range of end-use markets. The current demand softness is not isolated it is a broad-based withdrawal across all major consuming sectors, amplifying the downward pressure on prices.

Feedstock Pressure: Propylene Leads the Way Down

Propylene prices in China, which represent the key feedstock contributing to PO manufacturing costs, have fallen notably from the peak levels recorded during the first half of April 2026, when prices were close to $1,387 per metric ton. The correction in upstream propylene has removed one of the key cost-floor supports for PO, enabling sellers to discount without entirely sacrificing margins.

Operating rates at PDH (Propane Dehydrogenation) facilities continue to remain elevated due to relatively stable LPG feedstock costs, which has helped maintain adequate propylene supply availability in the market. Steam cracker co-product propylene from ethylene-oriented crackers adds further availability. This structural supply adequacy upstream translates directly into a softer PO cost floor.

Market Sentiment and Trading Activity

Market participants reported subdued buying activity across both spot and contractual markets during the period. Demand inquiries from polyol and propylene glycol manufacturers weakened compared to the previous week, prompting sellers to offer greater pricing flexibility to secure transactions. In addition, rising inventories at major Chinese port storage facilities indicated ample material availability, limiting the possibility of a strong short-term price rebound.

Downside Pressures: Short-Term Market Weakness

- Buyers in the downstream polyurethane foam and propylene glycol sectors continue following highly conservative, demand-driven purchasing patterns, with no visible stock-building activity ahead of potential seasonal improvement.

- Propylene feedstock values have eased steadily since the highs recorded in April, weakening upstream cost support and creating room for additional softening in PO pricing.

- Spot availability remains comfortable due to sufficient domestic supply alongside incoming import volumes, leading suppliers to lower offers to reduce inventories.

- A possible Q3 inventory replenishment phase among polyurethane manufacturers, especially if construction activity strengthens through economic stimulus measures, could help stabilise the market and support a mild rebound.

- Improved export economics for Chinese PO derivative products such as polyols and PG, driven by reduced production costs, may encourage higher plant utilisation and create indirect demand support.

China's propylene oxide market has completed a full round-trip from its March 2026 lows to an April peak and back. The current price level of $1,391.8 per MT (FOB China, May 21) reflects a market in equilibrium at reduced activity neither in freefall nor recovering. The path of least resistance remains downward in the near term, with buyers in control and sellers accommodating. A genuine recovery requires downstream demand normalisation, feedstock support, or a meaningful reduction in spot availability none of which appear imminent as of late May 2026.