-b_Big.jpg "MTBE Market Volatile Amid Feedstock Swings and Supply Risks")

The global Methyl Tert-Butyl Ether (MTBE) market has experienced a volatility during 2026, supported by occasionally buying gasoline blending economics, seasonal fuel demand, and lower refinery operating rates. MTBE remains one of the most important gasoline octane enhancers used by refiners worldwide to improve fuel quality and meet performance specifications. As high transportation cost activity across major economies, demand for gasoline blending components such as MTBE has strengthened considerably. At the same time, fluctuations in upstream prices, changing refinery margins, and geopolitical developments have contributed to increased market volatility.

MTBE’s recent pricing trends indicate a substantial rebound across key global markets. Cost and Freight (CFR) India MTBE prices rose from approximately $320 per MT in late February to $575 per MT by the end of May, reflecting an increase of nearly 80 per cent. Similarly, CFR Southeast Asia prices rose from $345 per MT to $612 per MT, while Free on Board (FOB) US Gulf values climbed from $460 per MT to $826 per MT during the same period. The US market witnessed the sharpest price spikes, touching as high as $933 per MT in early May before correcting lower. In contrast, CFR China prices increased from $281 per MT to $394 per MT, a relatively modest gain of about 40 per cent, reflecting the impact of abundant domestic supply and persistent export availability.

Highly Volatile Upstream Market Prices

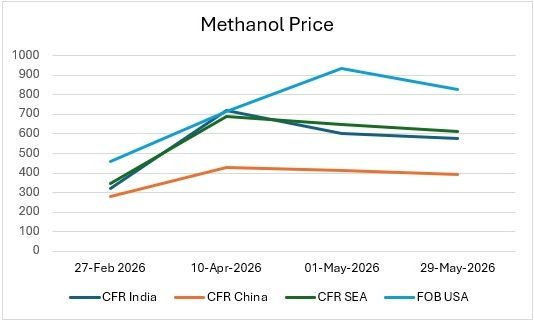

Methanol prices witnessed a substantial increase during the first half of 2026, reflecting the market's response to geopolitical disruptions and tightening supply conditions. Compared to February 27, 2026, CFR India prices rose by 80 per cent from $320 per MT to $575 per MT by May 29, 2026, while CFR Southeast Asia increased by 77 per cent from $345 per MT to $612 per MT. FOB US prices also surged by 80 per cent, moving from $460 per MT to $826 per MT, indicating that the impact was not limited to Asia but was felt across the global methanol market. CFR China increased by a comparatively lower 40 per cent, from $281 per MT to $394 per MT, largely due to China's ability to partially offset import disruptions through its domestic coal-based methanol production.

MTBE Demand Driven by Gasoline Blending and Refining Economics

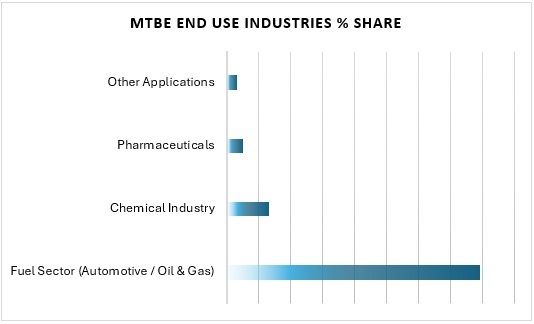

The transportation fuel industry remains the primary consumer of MTBE, with gasoline blending accounting for the largest share of global demand. Refineries incorporate MTBE into gasoline formulations to enhance octane ratings, improve fuel performance, and ensure smoother engine operation by minimising knocking. In emerging economies, where vehicle fleets continue to expand and fuel quality standards are becoming more stringent, MTBE remains a widely used and economical blending component for producing high-octane gasoline.

The MTBE market is closely connected to developments in the refining sectors. Although MTBE prices do not always move in tandem with upstream, the product's manufacturing process relies heavily on refinery-derived feedstocks and methanol, one of its key raw materials. Fluctuations in upstream prices influence feedstock costs, while elevated methanol prices can further increase MTBE production expenses and provide additional support to market values. When gasoline margins improve and refiners increase fuel production to capture stronger returns, demand for octane-boosting additives such as MTBE generally rises. As a result, MTBE pricing is determined by a combination of feedstock costs, methanol economics, refinery operating conditions, and trends in the global gasoline market.

The competitive landscape of the MTBE industry is increasingly shaped by refinery integration, feedstock availability, and regional export capabilities.

Saudi Basic Industries Corporation (SABIC) remains one of the world's most influential producers, benefiting from world-scale operations in Saudi Arabia's Jubail industrial complex. Its access to competitively priced C4 feedstocks provides a structural cost advantage, enabling the company to remain a major exporter to both Asian and European markets.

In China, Sinopec continues to dominate domestic production and remains the largest MTBE producer globally on a country basis. Multiple refinery-integrated facilities and ongoing capacity additions have strengthened China's position as the world's primary source of MTBE exports. However, this rapid expansion is also contributing to persistent oversupply concerns that continue to pressure regional pricing.

LyondellBasell remains a leading participant in the Western MTBE market through its oxyfuels business segment. The company benefits from flexibility between MTBE and ETBE production, allowing it to optimise margins in response to changing gasoline blending economics. Strong demand for high-octane fuel components has supported profitability across its oxyfuels portfolio.

In India, Reliance Industries plays a critical role in domestic supply through its Jamnagar refining and petrochemical complex. As India's transportation sector continues to expand and BS-VI fuel standards require higher-quality gasoline blends, Reliance remains strategically positioned to serve growing domestic MTBE demand while reducing import dependence.

South Korea's LG Chem strengthened its position in 2024 through capacity expansions targeting Asia-Pacific growth markets. The company has increasingly focused on high-purity MTBE grades used in chemical derivative applications, allowing it to diversify beyond traditional fuel blending demand.