-b_Big.jpg "Hydrofluoric Acid Prices Surge 23% Before Demand-Led Pullback")

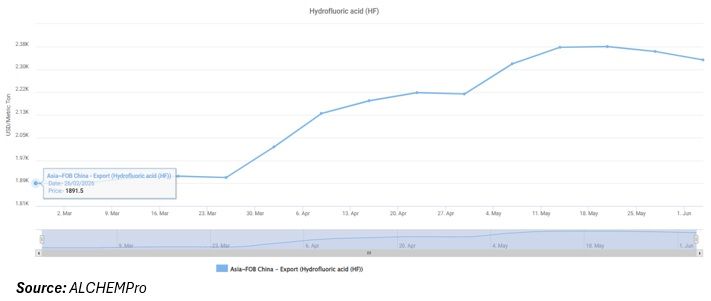

Hydrofluoric acid (HF) prices rose steadily over several months, supported by increasing raw material costs and healthy demand from key downstream sectors, before losing momentum as buyers became increasingly reluctant to transact at elevated price levels. HF prices registered a cumulative advance of approximately 23 per cent, rising from $1.891/kg in mid-February to a cycle peak of $2.377/kg on May 21, 2026, before beginning a measured correction in the final two assessment weeks.

Phase I: Baseline Stability (February–March 2026)

HF prices opened the year in a relatively tight range, holding at $1.891/kg through February before registering a modest uptick to $1.912–$1.917/kg through mid-March. This period of near-stasis reflected a market operating in relative balance, with demand from refrigerant ahead of the summer cooling season beginning to provide directional support, even as buyers adopted a wait-and-see posture ahead of anticipated upstream cost movements.

Phase II: Accelerating Uptrend

From the week of March 26, when HF prices surged from $1.912/kg to $2.021/kg in a single assessment a 5.7 per cent jump representing a meaningful step-change in market tone the uptrend became firmly established. Prices pressed higher through April and into May, advancing through $2.14/kg (April 09), $2.185/kg (April 16), and $2.214/kg (April 23), before accelerating to $2.316/kg on May 07 and $2.375/kg on May 14. This ascent was driven by a convergence of cost-push factors: elevated raw material procurement costs reflecting Chinese supply constraints imposed by mining consolidation and shutdowns; firm sulphuric acid input costs amplified by US-Iran war impacting sulphur supply chains from the Middle East; and sustained downstream seasonal stocks.

Phase III: Peak and Post-Peak Reversal (May 21–June 04, 2026)

The cycle peak was reached on May 21, 2026, at $2.377/kg, followed by the first meaningful sequential decline to $2.360/kg on May 28 (-0.7 per cent) and a further correction to $2.330/kg on June 04 (-1.3 per cent). While the absolute price decline remains modest in percentage terms thus far, the directional shift is analytically significant marking the transition from a seller-driven, cost-pushed bull market to a buyer-led phase of demand resistance. Downstream converters and trading houses, unwilling to commit to forward inventory at historically elevated levels, began stepping back from spot procurement, preferring hand-to-mouth purchasing strategies. This buyer passivity, by reducing spot offtake, has allowed inventory to accumulate at producer and trading levels, softening transactional prices.

Upstream Feedstock Analysis: The Dual Squeeze on HF Economics

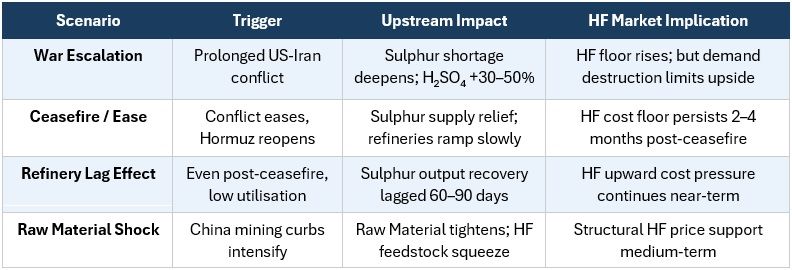

Despite the recent correction in HF prices from the cycle high of $2.377/kg on May 21 to $2.330/kg on June 04, developments in upstream feedstocks suggest that downward momentum may remain limited. After consolidating near $313/MT for several weeks, China's sulphur prices have resumed their upward trajectory, rising to $320/MT this week, signalling renewed cost pressure for sulphuric acid producers. In contrast, raw material prices have eased, providing some relief to HF manufacturing costs. However, given that sulphuric acid accounts for a portion of HF production economics, the recent rise increase in sulphur values could partially offset the benefit of raw material costs. It is anticipated that sulphur price will be higher in H2 2026.

Although HF prices have softened in recent weeks as buyers reduced spot purchases at elevated levels, the broader market outlook for the second half of 2026 remains tilted to the upside. Recent price corrections appear more reflective of short-term demand caution than a fundamental easing of production economics. Sulphur prices in China have resumed their upward movement after a brief consolidation period, while sulphuric acid values remain substantially above first-quarter levels. At the same time, raw material supply continues to face structural constraints linked to mining controls and environmental policies in China.

As a result, HF producers are likely to continue operating against a relatively high-cost base, limiting the scope for sustained price declines. Any improvement in refrigerant, fluoropolymer, or specialty chemical demand during H2 2026 could quickly tighten market conditions and support a renewed upward movement in HF prices. Even if geopolitical tensions ease, feedstock availability and supply-chain normalisation are expected to take time, suggesting that HF values may find stronger support later in the year.