(1)-b_Big.jpg "Ammonium Nitrate Climb Steadily as Supply Tightness Shows No Relief")

Ammonium nitrate (AN) remains one of the most strategically critical nitrogen-based chemicals globally, serving as the backbone of agricultural fertilisation and industrial explosives. In the period from March to June 2026, the global ammonium nitrate market has experienced significant turbulence driven by a convergence of geopolitical shocks, supply-side disruptions, and sustained agricultural demand. This report provides a comprehensive qualitative and quantitative assessment of AN price dynamics, weekly and regional trends, global production distribution, and near-term market outlook.

The Asia Free on Board (FOB) China ammonium nitrate export pricing displayed the most pronounced stable upward trajectory throughout H1. In the first week of March 2026, prices were recorded at approximately $0.510/kg, reflecting a stable baseline condition influenced by moderate pre-season demand from South and East Asian agricultural importers.

By the third week of March, a distinct inflection occurred as the Russia export suspension news broke (March 21–24, 2026), triggering immediate buyer anxiety in Asian import markets. Prices escalated sharply to the $0.60–$0.62/kg band during late March and early April, driven by panic procurement and inventory-building. This phase represents the most volatile weekly swing of the entire reporting window, with intra-week price movement of $0.04–$0.06/kg.

Through April and into May, prices stabilised in the $0.62–$0.64/kg range as the initial panic subsided but structural supply tightness persisted. The final recorded price as of May 31, 2026, stood at $0.641/kg the period high signalling that the market had not yet found downward relief from either resumed Russian exports or alternative supply channels.

2.2 Europe-FOB Europe Export Prices

The European ammonium nitrate export market, while exhibiting the same directional trend as Asia, showed notably more measured weekly price movements. Beginning March 2026 at approximately $0.407/kg, prices began a steady sequential climb reflecting Europe's position as the world's largest producing region (49 per cent of global output) which afforded some natural supply buffer against external shocks.

European prices displayed a more linear and less volatile weekly profile compared to the Asian channel. The rate of increase was approximately $0.005–$0.010/kg per week during the March–April window, accelerating only mildly in late April when post-Russian-quota demand from non-traditional European importers created short-term tightness.

By May 31, 2026, FOB Europe prices had settled at $0.499/kg a level reflecting the cumulative impact of input cost pressures (primarily natural gas for ammonia synthesis) and export demand from buyers pivoting away from Russian-origin material.

The persistent spread between Asia and Europe prices (approximately $0.142/kg as of May 31) reflects the structural cost advantages of European domestic production, where producers such as Yara International and EuroChem benefit from established ammonia supply infrastructure, though European natural gas price volatility has historically caused the greatest intra-year price swings in this region.

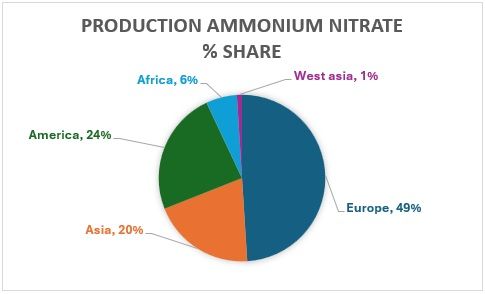

Regional Production Share Overview

The global ammonium nitrate production landscape is highly concentrated, with Europe and Russia collectively accounting for most of the world output. According to current production share data, the distribution is as follows:

Europe Dominant Production Hub

Europe's commanding 49 per cent share of global ammonium nitrate production reflects decades of industrial investment in nitrogen chemistry infrastructure. Major producers including Yara International (Norway), EuroChem (Switzerland/Russia-linked) operate large-scale facilities with integrated ammonia-to-nitrate production chains. European production economics are, however, tightly coupled to natural gas prices natural gas being the primary feedstock for steam methane reforming to produce ammonia, the precursor to ammonium nitrate.

The EU's Nitrates Directive (91/676/EEC) and the newly adopted RENURE amendments (February 2026) introduce further regulatory layering, particularly around the application rates of nitrogen-based fertilisers. While these regulations do not directly cap production, they introduce demand-side constraints that influence European producers' capacity utilisation and export orientation.

China's Export Competitiveness

Asia accounts for 20 per cent of global AN production, with China as the dominant producer within the region. The competitiveness of China's manufacturing and agricultural sectors is strengthened by extensive chemical production networks and public policies that influence the cost of key farming supplies. The FOB China export price of $0.641/kg as of May 31, 2026, reflects China's ability to command a premium in the export market during periods of global supply tightness, despite domestic cost structures that are generally more favourable than European equivalents.