-b_Big.jpg "Urea Prices Retreat Sharply After April 2026 Geopolitical Peak")

The urea granular market has traversed between March and June 2026 moving from a sustained multi-week surge driven by geopolitical shocks into a sharp correction phase that is now accelerating. The price rally, which pushed multiple region prices above $0.75–0.83/kg by early April, was rooted in supply disruptions across the Middle East, China's continued export restriction posture.

Early March (Weeks of March 2–March 9, 2026)

Urea granular prices clustering in the $0.44–0.46/kg range across most major routes. The Asia Cost and Freight (CFR) Southeast Asia import route was trading near $0.47/kg, the Europe Free on Board (FOB) Baltic export around $0.44/kg, and the US FOB US Gulf barge route at a discount to the rest of the pack, near $0.39–0.40/kg. The Middle East FOB Asia export benchmark was similarly priced in the $0.47/kg corridor.

Market sentiment at this point was already leaning bullish. The West Asia conflict had disrupted LNG flows through the Strait of Hormuz, squeezing feedstock availability for major producers in Qatar, the UAE, and Saudi Arabia. Pre-planting demand from India and Southeast Asia was building, and China had yet to signal any meaningful relaxation of its export quota restrictions, which had been in place since late 2025. These factors collectively put the market on alert for an upward price move.

Late March (Weeks of March 23–March 30, 2026)

The market surged further through the final week of March. The Asia CFR route crossed $0.727/kg, a level not seen since 2022, while the Europe FOB Baltic route advanced above $0.664/kg.

Buyer urgency accelerated. Agricultural importers across Southeast Asia and Brazil began securing pre-emptive coverage in anticipation of further tightening. The Middle East FOB Asia export route, constrained by supply-side bottlenecks, traded near $0.680/kg at month-end.

First Half of April (Weeks of April 6–April 13, 2026)

April marked the zenith of the 2026 urea price cycle. By the week of April 6, the Asia CFR SE Asia route peaked near $0.80/kg, with Europe FOB Baltic and South America CFR Brazil routes converging in the $0.71–0.76/kg band. The Middle East FOB Asia export benchmark reached approximately $0.72/kg. FOB Middle East granular futures were quoted around $763/MT, while US Gulf futures for the same period traded at $700/MT.

The combination of supply constraint, strong demand, and risk premiums for supply chain uncertainty created what the market described as a 'perfect storm' for nitrogen prices.

Early May (Week of May 4, 2026)

The week of May 4 was a clear inflection point. All five major routes charted a coordinated pullback, with the Asia CFR SE Asia route dropping from its $0.83/kg peak toward $0.810/kg, and the US Gulf barge route retreating sharply to approximately $0.616/kg. The Europe FOB Baltic, which had briefly touched $0.76/kg, pulled back toward $0.729/kg. The Middle East FOB Asia export route declined to around $0.77/kg peak toward $0.674/kg

The correction reflected a combination of seasonal demand softening, cautious restocking posture from buyers who had already secured coverage, and early whispers from trade sources about potential Chinese export quota resumption. Though no official announcement had been made by Beijing, forward market participants began pricing in the possibility of additional Chinese tonnes entering the global supply chain.

Mid-May (Weeks of May 11–May 18, 2026)

The correction deepened through May. By mid-month, the Asia FOB Middle East Asia export route had fallen to approximately $0.597/kg, representing a more than 25 per cent decline from its April peak a striking reversal. The South America CFR Brazil route eased toward $0.695/kg, and the US Gulf barge benchmark settled near $0.56/kg. The Europe FOB Baltic route remained relatively firm at $0.729-705/kg, partly supported by seasonal European agricultural demand and tighter logistics compared to other origins.

The Asia CFR SE Asia route traditionally the bellwether for the global urea complex stabilised around $0.810-$766/kg, suggesting the market had found a near-term support level.

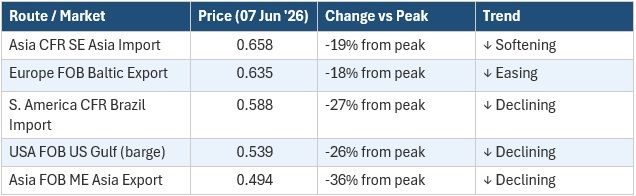

Europe FOB Baltic and Asia CFR SE Asia diverging positively from the other routes, with the former holding near $0.635/kg and the latter near $0.658/kg as of June 7. In contrast, the Middle East FOB Asia export route continued to soften, settling at $0.494/kg. The US Gulf barge route held near $0.539/kg, while South America CFR Brazil eased to $0.588/kg.

The market tone by early June was one of cautious watching rather than active buying or selling. Participants were awaiting clarity on the two most critical variables: the pace of Chinese export quota releases and the result of India's latest NFL tender. Both variables broke decisively in the same week adding to the conviction that the price correction still has further to run.

Price Outlook: Significant easing in prices was considered unlikely until China resumed active participation in the market. With Chinese exports returning and demand from India strengthening, the market is expected to witness further downward pressure on prices during the third quarter of 2026.

Subsidy Pressure in India: The country's fertiliser subsidy requirement, initially estimated at around ₹1.7 trillion for FY27, is now anticipated to rise substantially potentially reaching ₹3.4 trillion following the surge in fertiliser prices triggered by disruptions in West Asia earlier this year. At the same time, domestic urea producers continue to receive stable natural gas supplies, with current allocations meeting nearly 98 per cent of their average consumption levels over the last six months.