Oil surges amid geopolitical tensions

The OPEC has indicated a phased increase in crude output from the coming month nearly 206,000 barrels per day, aiming to stabilise market fundamentals despite ongoing geopolitical uncertainty.

Nearly 20 per cent of global seaborne crude and condensate trade transits through the Strait of Hormuz, while more than 40 per cent of India’s crude import volumes are routed via this strategic chokepoint. This concentration of supply flows underscores India’s elevated exposure to geopolitical disruptions, freight volatility, and logistical bottlenecks across Middle Eastern energy corridors.

Meanwhile, Brent Crude has strengthened above to 9 per cent, currently touched the level of near $82.4 per barrel, driven by rising geopolitical risk premiums and tighter prompt market sentiment. In the event of sustained escalation or physical supply constraints, crude prices could move toward the $100 per barrel range, supported by precautionary stocking, speculative positioning, and supply-side compression.

Any geopolitical tension involving regional powers significantly elevates risk perception among traders, insurers, and shipping companies operating through this corridor.

This heightened risk environment typically results in:

Middle East position in the global chemical ecosystem

Middle East has developed a strong petrochemical base focused on export-driven growth. Its competitive advantage lies in access to low-cost natural gas, which supports large-scale production of methanol, olefins, and nitrogen-based fertilisers.

Key export-oriented chemical segments

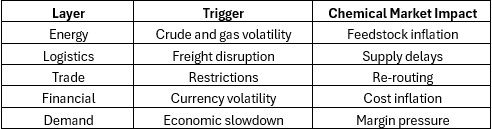

The impact of geopolitical tensions is not direct but spreads through multiple economic and industrial layers.

Multi-layer shock transmission

This layered structure explains why even localised tensions can influence global chemical pricing.

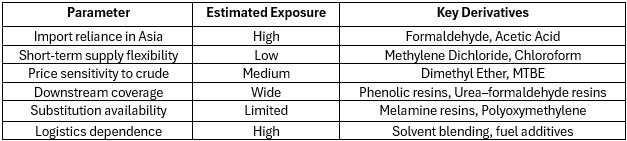

Quantitative risk exposure by key chemical chains

Methanol plays a central role in downstream chemical production. Countries in Asia, especially India and China, depend on imports for a large portion of their requirements. In recent days, methanol prices in India have surged by around 13 per cent, driven by tighter availability, higher logistics costs, and elevated geopolitical risk across Middle Eastern supply routes.

Methanol risk metrics

Market impact

Any supply disruption in methanol can quickly influence downstream industries such as laminates, pharmaceuticals, construction chemicals, and solvent-based manufacturing.

Fertiliser Chain: fertilisers exports from Gulf countries depend on maritime movement via the Strait of Hormuz.

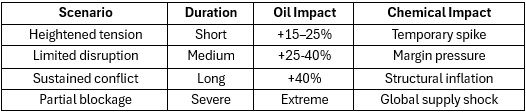

Market reaction under different levels of disruption

Conclusion

The Israel–US–Iran conflict represents a structural risk to the global chemical ecosystem. The most vulnerable areas include methanol, fertilisers, and crude-linked petrochemicals. Asia and emerging economies remain the most exposed.

In the long term, the industry is expected to transition toward diversified sourcing, regional supply chains, and integrated production models.

ALCHEMPro News Desk (VK)

Receive daily prices and market insights straight to your inbox. Subscribe to AlchemPro Weekly!