Impact on the textile and apparel industry

The closure or militarisation of the Strait would significantly impact the textile and apparel industry, which depends heavily on globalised supply chains for raw materials and finished products. Key consequences include:

Surge in energy prices

Disruption of maritime logistics

Risk to raw material supply from the Gulf

Trade uncertainty for yarn and fabric exporters

Strategic outlook

If prolonged, the Strait of Hormuz disruption could reshape trade flows and force buyers to reconsider sourcing strategies, such as:

For the textile industry, the conflict underlines the importance of supply chain resilience, multi-origin sourcing, and investment in localised recycling and synthetic alternatives.

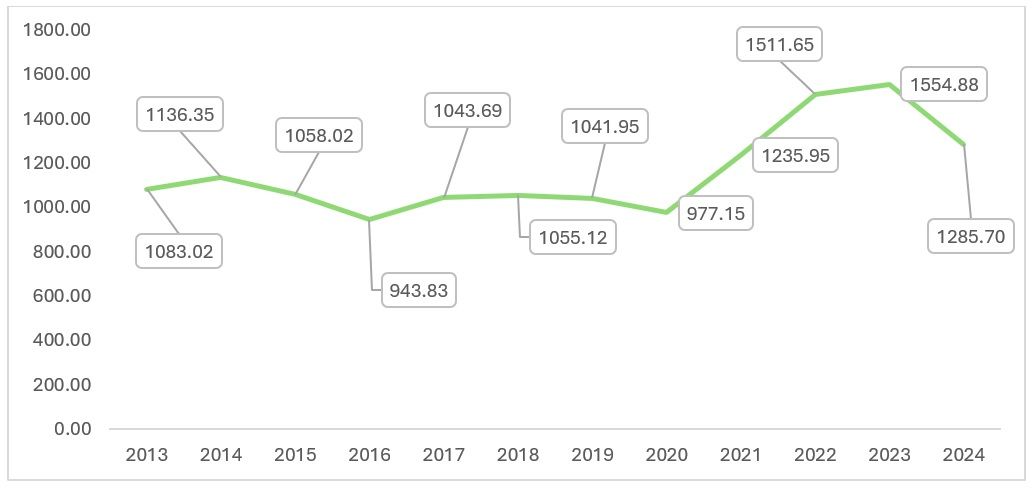

Exhibit 1: Middle East textile and apparel imports from the world (In $ bn)

Source: TexPro

Middle Eastern imports of discretionary items are largely dependent on world economic conditions, which in this decade have been marred by the pandemic as well as geopolitical tensions. Textile imports in the region reached their lowest during the peak pandemic period of CY 2021, with imports worth $977.15 entering the market. The recent decline in CY 2024 was due to the ongoing tensions between Israel and Iran, which caused imports to fall from a peak of $1,554.88 billion in CY 2023 to $1,285.70 billion—a reduction of 17 per cent. The current year also does not look good for textile and apparel imports due to continued unrest in the Middle Eastern region.

Major port disruptions and global impact on textile and apparel imports

Under the PortWatch simulation, major ports in Iran, the UAE, and Qatar are identified as being affected by the closure of the Strait of Hormuz. These ports serve as key transhipment hubs for several European and Asian countries, and a simulated 30-day disruption is projected to significantly impact textile and apparel imports across these regions.

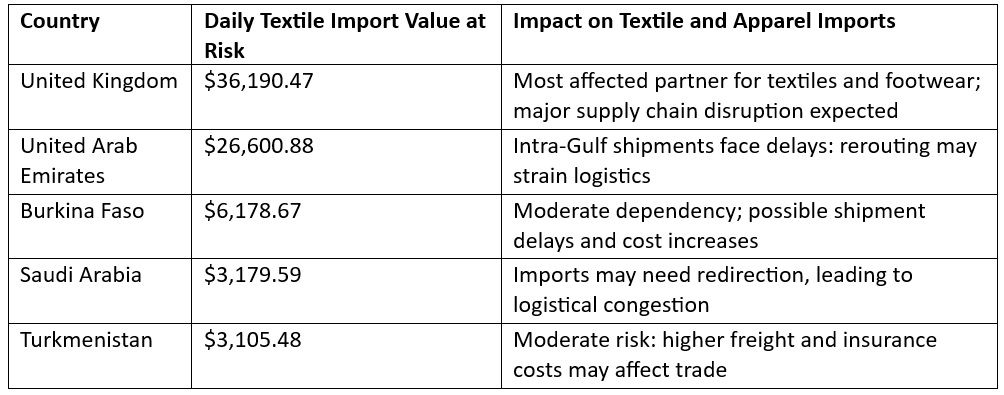

Table 1: Jebel Ali Port - United Arab Emirates

Source: PortWatch

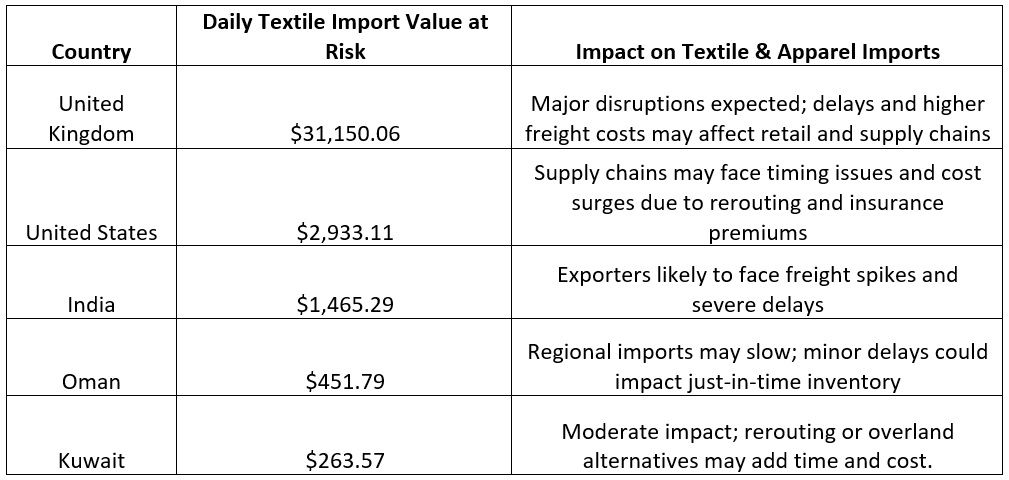

Table 2: Ras Laffan - Qatar

Source: PortWatch

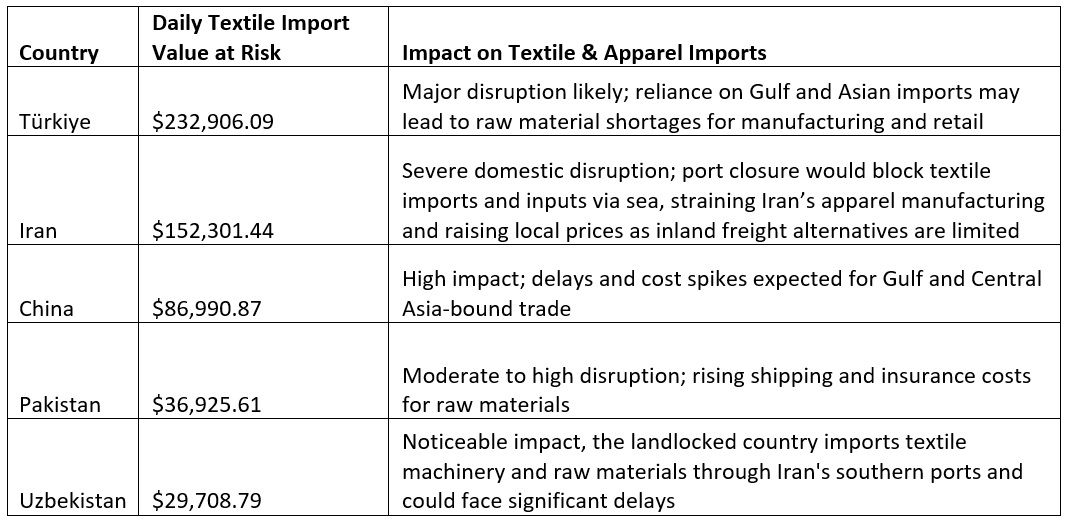

Table 3: Port of Shahid Rajaee (Bandar Abbas) - Iran

Source: PortWatch

The ongoing Iran–Israel conflict and the resulting threat of a potential closure of the Strait of Hormuz have introduced major disruption to global maritime trade flows. A simulation projecting a 30-day import delay using the IMF’s PortWatch reveals substantial expected congestion at key regional ports, particularly Jebel Ali in the UAE, Ras Laffan in Qatar, and Shahid Rajaee in Iran. These ports serve as critical transit points for containerised and energy-related cargo, especially from the Indian subcontinent and the Middle East to Europe and North America. The delay would not only disrupt container movements but also trigger cost inflation across logistics operations, with ripple effects on multiple economies tied to these routes.

Among the most adversely affected countries would be the United Kingdom, which depends significantly on textile and apparel imports from Bangladesh, Pakistan, and India. The majority of these shipments pass through Middle Eastern ports and the Strait of Hormuz, placing them at direct risk of delay or diversion. The increase in shipping costs, congestion surcharges, and extended lead times would reduce the cost-effectiveness of South Asian exports, especially when compared to competitors such as Vietnam. Furthermore, high logistical expenses could lead to lower volumes of trade, driving up prices in the UK’s domestic retail market. The UK may choose to source more from EU nations due to their proximity and trade agreements, albeit at the disadvantage of higher prices but superior quality.

The United States is another key economy likely to experience trade challenges from the closure. Ras Laffan in Qatar is a crucial hub for gas exports, but the broader disruption would affect the movement of goods from Egypt, China, and India as well. These delays could impact the timely arrival of textile shipments, which are essential to the US apparel sector. The US market, which relies heavily on just-in-time deliveries and efficient supply chains, would feel the strain in both import costs and reduced availability of goods, particularly during peak retail seasons. Delays would further complicate financial flows for suppliers in Asia and Africa, who often rely on fast invoice settlements to continue production cycles.

India occupies a unique position in this crisis, functioning as both a major exporter and an importer of key raw materials and high-quality finished textile goods. The Middle Eastern shipping corridor serves as a vital link for India’s trade with the European Union and the United States. Any obstruction in this corridor not only affects exports but also delays inbound shipments essential for India’s textile and apparel manufacturing ecosystem. While India has invested in developing the Chabahar port in southern Iran to bypass the Strait of Hormuz, the current scale and infrastructure of the port remain insufficient to absorb large volumes diverted from other regional ports.

A significant economic consequence of the Strait’s closure would be the rise in global crude oil prices. As the Strait is a key artery for oil and gas exports from the Gulf, any prolonged disruption would create a supply shock. The textile and apparel industry—especially the segment dependent on man-made fibres (MMFs)—is directly exposed to oil price volatility. An increase in crude prices would lead to higher production costs for synthetic fibres, dyes, and energy-intensive processes by about 10 to 20 per cent.

The disruption at Iran’s own port of Shahid Rajaee (Bandar Abbas) would have repercussions for emerging Asian economies that depend on the port for imports. Pakistan would be especially affected due to its reliance on key raw material imports for manufacturing finished goods.

The potential closure of the Strait of Hormuz would disrupt trade flows at a structural level, severely impacting port operations, supply chains, and global apparel distribution networks. The United Kingdom and the United States, as major textile and apparel importers, stand to incur substantial economic and trade-related losses. India, despite efforts to diversify routes via the Chabahar port, would face considerable challenges due to both its export reliance and import dependencies. The broader textile sector would contend with increased raw material costs, delayed shipments, and liquidity constraints, leading to price escalation and production instability across key markets.

Conclusion: Strategic implications for the global textile ecosystem

The unfolding geopolitical crisis involving the Iran–Israel conflict and the potential closure of the Strait of Hormuz poses a systemic risk to global trade, with far-reaching consequences for the textile and apparel industry. The chokepoint’s strategic significance for both energy flows and maritime logistics means that even temporary disruptions can trigger cascading effects across global supply chains.

Key textile-importing nations such as the United Kingdom and the United States are particularly vulnerable, given their reliance on timely shipments from Asia via Middle Eastern ports. For the UK, the cost advantage of sourcing from South Asia could erode rapidly, while the US may see its finely tuned just-in-time supply networks destabilised—especially during high-demand retail cycles.

India, despite its geographic proximity and efforts to develop alternate trade routes like the Chabahar Port, remains deeply entangled in this disruption—dependent on both imported synthetic feedstocks and export corridors through the Gulf.

Perhaps most critically, a potential spike in crude oil prices would directly impact the man-made fibre segment, which underpins much of today’s fast fashion and technical textiles. As synthetic yarn production becomes costlier, both input prices and retail garment prices are likely to rise, squeezing margins across the value chain and compelling brands to revisit their sourcing and pricing strategies.

In this uncertain environment, textile stakeholders must accelerate investments in supply chain resilience, including:

Ultimately, the industry’s ability to adapt to geopolitical shocks will determine not only cost competitiveness but also its long-term resilience in an increasingly volatile global trade environment.

ALCHEMPro News Desk (NS)

Receive daily prices and market insights straight to your inbox. Subscribe to AlchemPro Weekly!