India is the world's third-largest consumer of crude oil and one of the most import-reliant major economies for its hydrocarbon needs. This structural dependency is not a cyclical aberration, it is a function of geology, industrial scale and domestic energy transition. The data released by the Petroleum Planning & Analysis Cell (PPAC) for April–May FY2026-27 provides the clearest available snapshot of how this dependency is evolving, and the findings carry implications well beyond the energy sector. Crude oil import dependence stood at 88.7 per cent during the two-month reporting window. Translated into plain terms, India sourced approximately nine out of every ten barrels processed by its refineries from overseas suppliers.

Against this structural backdrop, the near-seven-percentage-point surge in energy's share of total merchandise imports from 19.6 per cent to 26.4 per cent is the single most consequential data point in the PPAC release. It signals that crude oil, LNG, and petroleum products now collectively account for more than one-quarter of everything India imports by value, a concentration that amplifies the macro-level sensitivity of the current account to global energy price movements and supply disruptions.

Import volume trends

India's crude oil procurement during April–May FY2026-27 totalled 41.7 million metric tonnes (MMT), a modest decline of 1.4 per cent compared with 42.3 MMT recorded in the corresponding two months of the prior year. While the directional trend is slightly favourable, the magnitude of the reduction is insufficient to meaningfully alter India's fundamental import exposure. The 88.7 per cent import dependence ratio, an improvement of only 1.2 percentage points from the 89.9 per cent recorded in April–May FY2025-26, underscores how difficult it is to move the needle on a structural reliance of this scale within a short time horizon.

The more movement was in petroleum product imports, which contracted by approximately 37 per cent, falling from 8.1 MMT to 5.1 MMT over the same comparative period. Combined crude and product imports for the two-month window totalled 46.9 MMT. On the export side, outbound petroleum product shipments declined 25.8 per cent, from 9.7 MMT to 7.2 MMT, reflecting softer international demand for Indian refinery output and shifting economics across global product trade routes.

Despite the reduction in crude intake, India's refining infrastructure demonstrated operational resilience. Total crude throughput during April–May FY2026-27 reached 43.4 MMT, compared with 45.2 MMT a year earlier a 4.0 per cent year-on-year decline, translating into an average processing rate of 5.22 million barrels per day (mb/d), down from 5.43 mb/d previously. Critically, petroleum product output of 44.6 MMT comfortably exceeded domestic consumption of 39.4 MMT, allowing refiners to sustain export volumes notwithstanding the year-on-year decline.

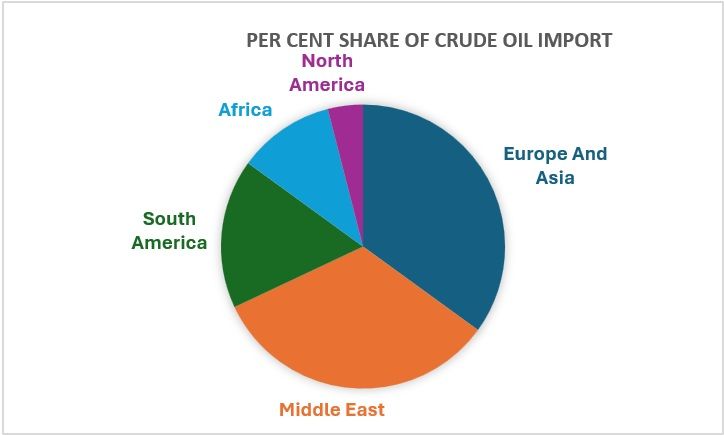

The crude processing mix remained largely stable: high-sulphur (sour) crude accounted for 33.0 MMT, or 76.1 per cent of total throughput, marginally down from 76.8 per cent in the prior period. Low-sulphur crude processing held steady at approximately 10.4 MMT, maintaining roughly a one-quarter share of total feedstock. This preference for sour crude reflects the sophisticated secondary conversion infrastructure, vacuum distillation units, hydrocrackers, cokers, and desulphurisation units that characterises India's complex refinery fleet, and which enables economic processing of discounted medium and heavy sour grades sourced from the Middle East, Europe and Asia

Softening Demand for Natural Gas Across the Value Chain The natural gas market followed a general trend of relaxing crude and product commerce. LNG imports decreased by about 20 per cent in April–May FY2026-27, falling from 5,643 million Standard Cubic Metre (MMSCM) in the same period last year to 4,532 MMSCM. Additionally, domestic natural gas production decreased slightly, adding 5,622 MMSCM to the supply mix. Over the two-month period, total gas usage was 10,075 MMSCM, indicating little activity in end markets like industrial and power generation. Domestic output is replacing imports, which suggests actual demand weakness, as shown by the concurrent decrease in both LNG imports and domestic production. The fertiliser industry, city gas distribution, industrial process heating, and thermal power generation are important sectors that utilise gas, and during the time frame, they seem to have operated at lower utilisation rates, which is in line with larger indicators of more moderate industrial output expansion in the Indian economy.

Shipping operators have been forced to divert tankers, especially through the longer Cape of Good Hope route, as a result of continuing US-Iran hostilities in and around the Red Sea, Black Sea, and sections of the Middle East. This has prolonged voyage durations by days or weeks and significantly changed the economics of crude and LNG transportation.

These interruptions result in a multi-layered cost load for Indian refiners, importers, and gas purchasers:

Partially insulates the country from supply shocks originating in a single source is India's sourcing strategy which has purposefully diversified across producers in the Middle East, West Africa, the Americas, Europe, and Asia. Nevertheless, the cost consequences of longer trip lengths cannot be completely negated by this geographic coverage. Once realistic freight and war-risk insurance costs are included in the feedstock's landed price, the economic appeal of discounted crude grades from distant or politically similar sources can be considerably diminished. The transmission route into retail gasoline pricing and domestic refinery economics is well-established and significant in light of India's energy usage, should these logistical cost constraints continue or worsen.

Particular attention should be given to the increase in energy's share of India's overall merchandise import value, which increased from 19. 6 per cent in April-May FY2025-26 to 26. 4 per cent in the same period of FY2026-27. A shift of nearly seven percentage points within a single year is not a rounding error; it is a structural signal.

This elevated energy import share has several macro-level implications. First, it concentrates current account vulnerability in a category of imports that is price-inelastic in the short run, India cannot rapidly reduce crude volumes without compromising refinery utilisation and domestic fuel supply. Second, it amplifies the rupee's sensitivity to global oil price movements, since a higher oil price simultaneously widens the trade deficit and pressures the currency, a well-documented feedback loop. Third, it crowds out fiscal and foreign exchange capacity that might otherwise support investment in non-energy imports, including capital goods, electronics, and industrial inputs.

In the context of India's broader ambition to expand manufacturing, reduce import dependence in strategic sectors, and internationalise the rupee, a structurally elevated energy import share represents a material constraint on the macroeconomic policy space available to policymakers.

Near-term resilience and long-term transition

Supply-side measures

India's energy security policy response operates across two distinct time horizons. In the near term, supply-side resilience is being strengthened through geographic diversification of crude sourcing across multiple producing regions, the Middle East, West Africa, the Americas, and Europe and Asia suppliers to reduce concentration risk.

Demand-side and structural transition

The more consequential policy lever over the medium to long term is the demand-side transition agenda includes:

Near-term improvements in the crude import dependence ratio are likely to remain modest, but the cumulative effect of sustained investment across renewables, biofuels, hydrogen, and electrification could meaningfully shift the structural picture by the early 2030s.

India's refining sector is demonstrating operational resilience, sustaining output above domestic consumption requirements even as throughput eases. The policy response spanning supply diversification, reserve building, and the long-term transition agenda is structurally sound, but the scale of the challenge means that import dependency at or near current levels will remain a defining feature of India's energy economy through the medium term. For energy sector analysts, policy planners, and financial markets participants, the central lesson is that the direction of India's energy transition is clear.

ALCHEMPro News Desk (DL)

Receive daily prices and market insights straight to your inbox. Subscribe to AlchemPro Weekly!